By Thomas D. Begley, Jr., CELA

A Third Party Special Needs Trust is usually used in a Medicaid context not for the benefit of the grantor of the trust, but for the beneficiary.

The grantor of the trust is typically a parent, but could be grandparent, sibling, other relative or friend. The grantor uses the grantor’s assets to fund the trust. The assets of the beneficiary cannot be used to fund a Third Party Special Needs Trust. In order for the trust to be a Special Needs Trust, the beneficiary must be disabled. Disability is usually determined ,y the fact that the beneficiary has received a Determination of Disability from the Social Security Administration and is receiving either Supplemental Security Income (“SSI”) or Social Security Disability Income (“SSDI”). The trust is designed so that the assets are not counted for Medicaid eligibility purposes. The beneficiary is then able to take advantage of the continuation of public benefits including usually SSI and Medicaid, as well as use the assets in the trust to enrich the beneficiary’s life. The trustee is given complete discretion with respect to distributions, and special needs language is used in designing the trust. Provisions made for distributions to the beneficiary during the beneficiary’s lifetime and distribution of any remaining principal and accrued income upon the death of the beneficiary.

Trustee

It is always good practice to select a professional trustee. The professional trustee has expertise with respect to public benefits law, tax Jaw, investment management, and usually has the ability to assist in navigating the disability system. Often the grantor of the trust is uncomfortable with a professional trustee, but this problem can usually be solved by appointing a family member as trust protector. The trust protector monitors the performance of the trustee and is given the authority to remove and replace the trustee. The trust protector’s power to remove and replace the trustee can be conditioned on cause, which would be defined in the trust document, or can be without cause. It is generally required that the replacement trustee be a professional with a certain amount of assets under management. In order for disability organization to qualify, the asset management limit might be as low as $50,000,000. On occasion, the grantor of the trust has worked with a financial advisor who would like to continue to be the financial advisor after the trust is established. Many professional trustees, such as Comerica Bank, have arrangements with money managers, such as Morgan Stanley or UBS, where Comerica will retain the outside money manager to invest the funds. This should be spelled out clearly in the trust document. The investment manager has an additional cost for managing the funds. The combined cost of the investment manager and the trustee usually exceeds the cost of having a professional trustee manage the funds in-house. This should be clearly understood by the client.

Alternatives to a Special Needs Trust

There a number of alternatives to Special Needs Trusts. These include the following:

- Disinherit a Child. The problem with this strategy is that one cannot be certain that public benefits, as we know them today, will continue forever. Many public benefits have been cut back in recent years and there is no guarantee that current benefits will not be reduced as well.

- Leave Money to the Child. The problem with this approach is that unless the funds being left to the child are very significant, they may not last long if the child’s needs, particularly medical needs, are great. It is usually better to maintain public benefits and establish a trust for needs or wants that will not be covered by public benefits.

- Leave Funds to Sibling. This is the common strategy that frequently backfires. The idea is to leave the share of the person with disabilities to a brother or sister with the understanding that the brother or sister will use that money to care for the child with disabilities. The problems occur when the child to whom the funds are left is sued by a creditor, is divorced, or simply says, “I want to use this money for myself. The Will says that I have to use it for my sibling with disability, but I am not going to use it for that purpose.” Sometimes it is the sibling that makes this decision, but frequently it is the spouse of the sibling who pushes for that result.

- Pooled Trust. A Pooled Trust is a good solution for relatively small amounts of money. If the trust is less than $100,000, Pooled Trust makes sense. If it is between $100,000 and $200,000, a Pooled Trust should be compared to a Third Party Special Needs Trust. If the amount involved is in excess of $200,000, a Third Party Special Needs Trust is almost always the best solution.

- ABLEAccount. New Jersey has adopted legislation authorizing ABLE accounts. These accounts are expected to come into existence sometime in the next few months. ABLE accounts are already in existence in several states, and some states, such as Ohio, permit out-of-state residents to open an ABLE account in that state. A problem is that not more than the gift tax annual exclusion amount can be contributed to an account in any one year and no beneficiary can have more than one account. The annual exclusion gift tax exemption for 2017 is $14,000. So, if the inheritance is $14,000 or less, an ABLE account might make sense.

Planning Considerations

Let’s examine the seven planning considerations in the context of a Third Party Special Needs Trust.

- Availability. Assets in a Third Party Special Needs Trust are not available for SSI or Medicaid purposes, because the Special Needs Trust gives the trustee sole discretion with respect to distributions and prohibits the beneficiary from revoking the trust. If the assets in the trust are not available, they are not counted for SSI or Medicaid eligibility purposes.

- Transfer of Asset Penalty. There is a transfer of asset penalty to the grantor for transfers to a Third Party Special Needs Trust. This is why a Third Party Special Needs Trust is seldom utilized in Medicaid planning for the grantor.

- Payback. A Third Party Special Needs Trust is not required to have a provision calling for payback to Medicaid for medical assistance paid on behalf of the trust beneficiary.

- Funding. Virtually all assets could be used to fund a Third Party Special Needs Trust. If retirement assets are being used, typically the trust is simply made the beneficiary of the retirement account upon the grantor’s death. Accumulation Trust language should be included. Beneficiary designations of life insurance, annuities or retirement accounts must be addressed. If part of the funds are going to healthy children, and part are going to the Special Needs Trust, consideration should be given to leaving the retirement accounts to the healthy children, rather than to the trust. Administration of a trust with a retirement account is somewhat complex, even for professional trustees.

- Tax Considerations

- Income tax. A Third Party Special Needs Trust can be designed as a grantor trust or a non-grantor trust.

- Gift tax. A Third Party Special Needs Trust can be designed as an IDGT or a non-IDGT.

- Estate tax. A Third Party Special Needs Trust can be designed so that the assets in the trust remain in the estate of the grantor or are excluded from the estate of the grantor.

- Estate Recovery. There is no estate recovery against the estate of the grantor of a Third Party Special Needs Trust or the beneficiary, so long as the grantor retains no interest in the trust.

- Elective Share. Assets in a Third Party Special Needs Trust would be subject to the elective share stature.

by Thomas D. Begley, Jr., Esquire, CELA

CMS has released the Medicare and Medicaid numbers for 2017. They are as follows:

Medicaid

- Income Cap[1] $2,205

- Maximum Community Spouse Resource Allowance (CSRA)[2] $120,900

- Minimum CSRA[3] $24,180

- Maximum Minimum Monthly Maintenance Needs Allowance (MMMNA)[4] $3,022.50

- MMMNA (July 1, 2016 until June 30, 2017)[5] $2,002.50

- MMMNA (July 1, 2017 until June 30, 2018)[6] $2,030.00

- Excess Shelter Allowance (July 1, 2016 until June 30, 2017)[7] $600.75

- Excess Shelter Allowance (July 1, 2017 until June 30, 2018)[8] $609.00

- Maximum Resource Limit (Individual)[9] $2,000

- Minimum and Maximum Cap on Equity in the Home[10] $560,000 – $840,000

Medicare

Part A

- Medicare Co-Payment – Skilled Nursing Facility (SNF)[11] $164.50

- Hospital Deductible[12] $1,316

- Per day Co-Insurance – Day 61 -90[13] $329

- Per day Co Insurance – Day 91-150[14] $658

Part A Premium (for voluntary enrollees only)

- With 30-39 quarters of Social Security coverage[15] $227

- With 29 or fewer quarters of Social Security coverage[16] $413

Part B

Medicare Part B – Single or Married and Filing Joint Return

Part B Income-Related Premium[19]

| Beneficiaries who file an individual tax return with income:

|

Beneficiaries who file a joint tax return with income: | Income-related monthly adjustment amount | Total monthly premium amount

|

| Less than or equal to $85,000

|

Less than or equal

to $170,000 |

$0.00 | $134.00 |

| Greater than

$85,000 and less than or equal to $107,000

|

Greater than $170,000 and less than or equal to $214,000 | $53.50 | $187.50 |

| Greater than $107,000 and less than or equal to $160,000

|

Greater than $214,000 and less than or equal to $320,000 | $133.90 | $257.90 |

| Greater than $160,000 and less than or equal to $214,000

|

Greater than $320,000 and less than or equal to $428,000 | $214.30 | $348.30 |

| Greater than $214,000 | Greater than $428,000 | $294.60 | $428.50 |

In addition, the monthly premium rates to be paid by beneficiaries who are married, but file a separate return from their spouse and lived with their spouse at some time during the taxable year are:

| Beneficiaries who are married but file a separate tax return from their spouse:

|

Income-related monthly adjustment amount | Total monthly premium amount |

| Less than or equal to

$85,000

|

$0.00 | $134.00 |

| Greater than $85,000 and

less than or equal to $129,000

|

$214.30 | $348.30 |

| Greater than $129,000 | $294.60 | $428.60 |

Standard Part D Cost-Sharing for 2017[20]

- Annual Deductible Maximum $400

- Member Pays 25% of the Next… $3,300 (25% = $825)

- Initial Benefit Period Maximum $3,700 ($400 + $3,300)

- Donut Hole Threshold $3,725

(Brand name drugs: 50% + 10% plan “subsidy,” Generic drug: 49% subsidy)

- Catastrophic Coverage $4,950 ($400 + $825 + $3,725)

- Catastrophic cost-sharing: Generic $3.30/$8.25 or 5% (whichever is greater)

- Catastrophic cost-sharing: Brand $7.40 or 5% (whichever is greater)

[1] 42 U.S.C. §1396a(a)(10)(A)(v); 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[2] 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[3] 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[4] 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[5] 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[6] 82 Fed. Reg. 8832 (Jan. 31, 2017).

[7] 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[8] 82 Fed. Reg. 8832 (Jan. 31, 2017).

[9] 20 CFR § 416.1205(c).

[10] 42 U.S.C. §1396p(f); 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[11] 81 Fed. Reg. 80062 (Nov 15, 2016).

[12] 81 Fed. Reg. 80062 (Nov 15, 2016).

[13] 81 Fed. Reg. 80062 (Nov 15, 2016).

[14] 81 Fed. Reg. 80062 (Nov 15, 2016).

[15] 81 Fed. Reg. 80072 (Nov 15, 2016).

[16] 81 Fed. Reg. 80071 (Nov 15, 2016).

[17] 81 Fed. Reg. 80063 (Nov 15, 2016).

[18] 81 Fed. Reg. 80063 (Nov 15, 2016).

[19] 81 Fed. Reg. 80066 (Nov 15, 2016).

[20] http://www.medicareadvocacy.org.

The post MEDICAID AND MEDICARE 2017 COLA NUMBERS first appeared on SEONewsWire.net.]]>A person who had a disability prior to age 26 may now setup an ABLE Account, and anyone may contribute to such account; provided, however, that total contributions to the account may not exceed $14,000. The person with the disability may use the money for “qualified disability expenses,” such as housing and basic living expenses. The utilization of the ABLE Account funds for such purpose will not be considered in-kind support and maintenance. To demonstrate the value of these accounts, I am going to use two common examples:

Parents Did Not Charge Rent: Ron’s Case

Ron is a 19-year old with Down Syndrome who lives with his parents. Ron just started to receive SSI; but, because his parents do not charge him for food or shelter, he receives a 1/3 reduction of his full benefit amount due to in-kind support and maintenance. The monthly household food and shelter expenses total $2,175, and because Ron is one of three people living in the house, he is responsible for a total of $725. Because of the reduction in income, Ron is unable to start paying his parents his pro rata share of the household food and shelter expenses. An ABLE Account is established for the benefit of Ron, and Ron’s parents contribute $2,000 to the account. Ron will pay his parents his $725 share of rent (from a combination of his SSI check and his ABLE Account). The rent payments will be reported to the Social Security Administration, and the Social Security Administration will then increase Ron’s SSI check to the full $735. To continue to receive the full benefit amount, Ron must continue to pay his parents rent. (Bear in mind that earned and unearned income may also factor into Ron’s benefit amount, but this is for a later discussion).

Household Expenses Too High: Jackie’s Case

Jackie is a 35-year old with Cerebral Palsy who lives with her sister. When Jackie moved in with her sister, her pro rata share of household expenses totaled $1,000 and the full SSI benefit was not sufficient to cover her pro rata share. As a result, Jackie received a 1/3 reduction in her benefit due to in-kind support and maintenance. Jackie established an ABLE Account and the Trustee of her Special Needs Trust distributed $5,000 to the account. Jackie can now pay her sister $1,000 to cover her pro rata share of the expenses (via SSI and her ABLE Account). The change in circumstances will be reported to the Social Security Administration who would then increase Jackie’s SSI check to the full $735 a month. From that point forward, Jackie’s Special Needs Trust will continue to distribute money into her ABLE Account so that she can continue to pay her pro rata share of household expenses and receive her full SSI check.

Ask Kit Kat – All About Skunks

Ask Kit Kat – All About Skunks

Hook Law Center: Kit Kat, what’s the latest information about skunks, and what should you do if your pet has encountered a skunk?

Kit Kat: Well, this can cause some problems you might not anticipate, though, generally, your pet’s encounter with a skunk can be quite harmless. Usually, the skunk gives some warning before employing its ultimate weapon—the spray. Initially, you may notice the telltale smell, but there may be other symptoms like drooling, sneezing, or vomiting. More severe symptoms can emerge a few days later like lethargy and pale gums. If the more severe symptoms appear, immediately take your pet to the vet to be checked. In most cases, the severer symptoms occur after a direct spray to the face.

Now, how to deal with cleaning your pet after a potent spray. Ordinary pet shampoo will not be strong enough. You will need to make your own mixture composed of 1 quart of 3% hydrogen peroxide, ¼ cup baking soda, and 1-2 tsps. of dishwashing liquid. Lather your pet well and let it sit for about 5 minutes. Then, thoroughly rinse with lots of water. If your pet has long hair, you may want to consider clipping them before shampooing, because a shorter coat will foster more effective results. There may be some bleaching of the fur with this procedure, but it is not harmful to them. Repeat as necessary.

To prevent your house/property from being attractive to skunks, there are several things you can do. First, if you store food in your garage/shed like bird seed or dry pet food, make sure it is in well-sealed containers. Second, make sure areas around decks are blocked, so they cannot make their home there. Third, keep exterior lights at night on or install motion-activated lights. Skunks do not like light. Fourth, discourage their nesting in your yard by sprinkling kitty litter in front of their den/hole or stuffing it with twigs and leaves. This will let them know, that they are not welcome.

Hopefully, with this knowledge, you will be well-equipped to handle your pet’s skunk encounter. If your pet is actually bitten, you should take your pet to a veterinarian right away. Skunks can carry rabies, and prompt medical attention could be crucial. (“Pets and Skunks: A Smelly Dilemma,” ASPCA Action, Issue #3, 2016, p. 8)

Distribution of This Newsletter

Hook Law Center encourages you to share this newsletter with anyone who is interested in issues pertaining to the elderly, the disabled and their advocates. The information in this newsletter may be copied and distributed, without charge and without permission, but with appropriate citation to Hook Law Center, P.C. If you are interested in a free subscription to the Hook Law Center News, then please telephone us at 757-399-7506, e-mail us at mail@hooklawcenter.com or fax us at 757-397-1267.The post Maximizing Your Child’s SSI by Utilizing ABLE Accounts first appeared on SEONewsWire.net.]]>

As a reminder, ABLE accounts are for blind or disabled individuals whose blindness or disability occurred before the individual’s 26th birthday and i) who are entitled to benefits under the Social Security Act (SSI or SSDI); or ii) who self-certify that they have a condition listed on the Social Security Administration’s list of compassionate allowances conditions and have a signed qualifying disability diagnosis from a qualified physician; or iii) who self-certify that they have an eligible disability and have a signed qualifying disability diagnosis from a qualified physician. ABLE accounts may be opened by the disabled individual in his/her own capacity if he or she is 18 years of age and competent to make financial decisions for him or herself. If the disabled individual cannot open the account independently, a guardian or attorney in fact acting under a valid durable power of attorney may open the account on the individual’s behalf. Parents can open such accounts on behalf of minors. All accounts can be opened online at able-now.com.

ABLE accounts, similar to the 529 education accounts they are modeled on, allow for contributions to grow free of federal and state income tax and for distributions for “qualified disability expenses” to be made free of federal and state income tax. A “qualified disability expense” is one which is incurred at a time when the individual is eligible (as described above), which relates to the person’s blindness or disability and which helps maintain or improve the person’s health, independence and quality of life. This standard is quite broad and can include education, housing, transportation, employment training and support, assistive technology, health, financial management, legal fees, funeral and burial expenses etc. It will be important to track and account for these expenses, because the total distributions from the account will be reported to the IRS annually. Maintaining detailed records and receipts will be an important part of administering an ABLE account. Failure to use the money in the ABLE account for a qualified disability expense (or to be able to prove such expense) will subject the withdrawal to a 10% penalty and the individual will include the amount of the withdrawal in his or her income. It is also possible that such non-qualified funds could be counted as income or as a resource for means-tested benefit programs. An important side-benefit of contributing to an ABLE account is that Virginia allows an income tax deduction of up to $2,000 per contributor.

ABLE accounts are limited in some very important ways. Contributions to an ABLE account are limited to the amount of the annual gift tax exclusion, currently $14,000/year. This limit applies to contributions from all sources, so the account cannot be used to shelter large sums of money. Furthermore, upon the death of the disabled individual, any balance in the ABLE account is subject to payback to Medicaid for funds paid by Medicaid on behalf of the disabled individual after the creation of the account. Finally, for disabled individuals collecting SSI, balances in an ABLE account in excess of $100,000 are counted as an asset for determining eligibility for SSI (but not for Medicaid eligibility). Although Virginia currently has a ceiling of $500,000 on the assets that can be in an ABLE account, ABLE accounts are not a substitute for Third-Party Special Needs Trusts or for First-Party Special Needs Trusts because of the limitations on annual contributions and the Medicaid payback requirement. However, they can function very well as an adjunct to a well-conceived plan to care for individuals with disabilities. An ABLE account can be a way to provide independence for some individuals who are able to manage their own financial affairs and may be an excellent repository for unexpected inheritances or for extra savings.

If you would like to discuss how to utilize an ABLE account in your planning for a person with disabilities, contact one of the experienced attorneys at the Hook Law Center so we can help you make sense of possibilities.

Ask Kit Kat – Sea Turtles in Danger

Ask Kit Kat – Sea Turtles in Danger

Hook Law Center: Kit Kat, what can you tell us about sea turtles in the Outer Banks and how they are faring during this cold patch of weather?

Kit Kat: Well, the sea turtles who overstayed their normal residency in the Outer Banks are having quite a time this winter. Temperatures have been unusually cold. Even though, the cold snaps don’t last for days on end, they are still a danger to these warm-water, loving creatures. According to Jeff Hampton of The Virginian-Pilot, “turtles cannot move when water temperatures fall below 50 degrees.” Most have left the area by now, but a few get fooled by a warm fall, and forget to leave to go south for the winter. Fortunately, for them, they got delayed in the right place to get expert treatment!

8 green sea turtles, one loggerhead, and one Kemp’s ridley turtle were rescued from the beaches of Pimlico Sound over the weekend of December 10-11, 2016. They were rescued by staff from the North Carolina Aquarium-Roanoke Island, volunteers from the Hatteras Network for Endangered Sea Turtles, and rangers from the National Park Service. The turtles were then treated at the aquarium’s rehabilitation center. It’s a slow process. They are gradually warmed by a rate of 5 degrees per day, until reaching their normal body temperature. The treatment involves administering fluids and analyzing their blood. Some even require antibiotics if they happen to also catch pneumonia. Once they are stabilized, they are released to a beach further south, but they must first be able to swim and eat normally.

This current rescue effort was quite small compared to last year. At that time, the rescue teams were overwhelmed with the number of turtles needing care when caught in a prolonged cold snap. Rosemary Lucas, coordinator of the rehabilitation center, said they had tubs of warming water all over the center—even in hallways and bathrooms. Contributions from the community help in these efforts. If you would like to donate to this cause, you may do so online at ncaquariums.com/roanoke-island with the code SEATURTLE2016. Contributions by check may be sent to NC Aquarium, 374 Airport Rd., P.O.Box 967, Manteo, NC 27954 with the notation of STAR or SEA TURTLE in the subject line. (Jeff Hampton, “Stunned by the cold,” The Virginian-Pilot, December 14, 2016, p. 4)

Distribution of This Newsletter

Hook Law Center encourages you to share this newsletter with anyone who is interested in issues pertaining to the elderly, the disabled and their advocates. The information in this newsletter may be copied and distributed, without charge and without permission, but with appropriate citation to Hook Law Center, P.C. If you are interested in a free subscription to the Hook Law Center News, then please telephone us at 757-399-7506, e-mail us at mail@hooklawcenter.com or fax us at 757-397-1267.The post ABLE Accounts Open in Virginia first appeared on SEONewsWire.net.]]>

By Thomas D. Begley, Jr., CELA

Trusts for disabled individuals who have not reached age 65 and are funded with assets of the disabled person are authorized under OBRA-93.(1) The trust is for the benefit of disabled persons. The person much be under 65 at the inception of the trust. While the trust must be established and funded prior to the beneficiary attaining the age of 65, it may continue after 65. If the trust is funded with a structured settlement prior to the beneficiary attaining the age of 65, the trust remains viable even though payments from the annuity are received after age 65.

The trusts must be established by a parent, grandparent, legal guardian, or court. Curiously, they cannot be established by the disabled individual. However, there is legislation in Congress that would permit the individual beneficiary to establish his or her own trust.

By statute, transfers to the trust are not subject to the transfer of assets rules. The trust should be drafted so that the resources are unavailable. The trust should be administered in such a way that the income is not counted as income to the beneficiary.

The trust must provide that on death the funds remaining in the trust go first to reimburse Medicaid and then for the benefit of other beneficiaries.

The assets used to fund the trust must be the assets of the beneficiary, not the assets of a third party, except that a token amount is permitted to be contributed by a third party to seed the trust, i.e., S10 or S20. If a trust is funded with assets of a third party, it is considered a Third-Party Special Needs Trust and the rules are very different. Generally a Self-Settled Special Needs Trust, or First-Party Special Needs Trust is used in connection with:

- A personal injury settlement

- An inheritance

- Child support

- Alimony

When drafting a Self-Settled Special Needs Trust, it is always good practice to use a professional trustee. Family members are always well intentioned, but do not have the necessary expertise with respect to public benefits law, tax law and investments and do not know how to navigate the disability system. Family members frequently have a conflict of interest with the beneficiary. Family members are often uncomfortable in naming a professional trustee. A way to make everyone happy is to appoint family member as trust protector. The trust protector is given the authority to monitor the trustee and to remove and replace the trustee, if the trust protector is dissatisfied with the trustee’s performance. The trust protector’s power to remove and replace could be limited to cause, which would be spelled out in the trust document, or the power could be exercised without cause. If a family member serves as trust protector, it is inappropriate to provide for compensation for the family member. The document should provide that if the trust protector removes and replaces the professional trustee, the new trustee must also be a professional trustee. The professional trustee could be a corporate trustee or a disability organization. It is good practice to set a limit on the dollar amount under management by the new trustee. Fifty million dollars might be appropriate, so that disability organizations can qualify.

Established by

A Self-Settled Special Needs Trust must be established by a parent, grandparent, guardian or court. The Social Security Administration (SSA) is now taking the position that if a parent establishes a trust, they must fund the trust with 510 of the parent’s money. This position is based on a court case, Draper v. Colvi11.(2) The rationale seems to be that the person who “first funds” the trust is the establishor. If the parent signs the trust, but funds it with the personal injury settlement, inheritance, child support or alimony, then that money belongs to the beneficiary of the trust, so the court

and Social Security are taking the position that the first funding comes from the beneficiary and the beneficiary is not permitted to establish a Self- Settled Special Needs Trust.

The same rationale would apply to a trust established by a grandparent. Self-Settled Special Needs Trusts are seldom established by a guardian, because court action is required to authorize the guardian to establish the trust. As a practical matter, it is easier to simply have the court establish the trust. The judge will not want to sign the trust, so the trust document must state that the trust is approved, required and established and the judge directs another individual to sign the trust. Typically, the individual signing the trust is the parent, but the first funding doctrine does not apply, because the trust is actually being established by the court. It is not good practice to simply incorporate the trust in the court order by reference. It is important that the judge direct someone to sign the trust. If a parent or grandparent is not available, it could be any other family member or even an attorney.

In establishing any trust to be used in a Medicaid context, there are seven planning considerations:

- Availability. Because the trust language gives the trustee total discretion as to distributions, the assets in the Self-Settled Special Needs Trust are not considered available for Supplemental Security Income (“SSI”) and Medicaid eligibility purposes. It is important to carefully draft the trust with appropriate special needs language.

- Transfer of Asset Penalty. There is no transfer of asset penalty for SSI and Medicaid, because there is a statutory exemption under 42 U.S.C. § 1392b and 42 U.S. C. § 1396p(d)(4)(A).

- Payback. A payback to Medicaid is required by law. The payback is for all medical assistance received by the beneficiary since birth. It is not sufficient to pay back Medicaid benefits received from the date of the establishment of the trust to date. In the case of a personal injury settlement, the Medicaid payback is not limited to medical assistance related to the personal injury.

- Funding. Self-Settled Special Needs Trusts are generally funded by personal injury recoveries, inheritances, equitable distribution, alimony or child support. However, any asset can be used to fund a Self-Settled Special Needs Trust.

- Tax Considerations

- Income. A Self- Settled Special Needs Trust is considered a granter trust. Therefore, the income earned by the trust is taxed to the beneficiary at the beneficiary’s tax rates.

- Gift. Transfers to a Self-Settled Special Needs Trust are not completed gifts.

- Estate tax. Assets in a Self-Settled Special Needs Trust are included in the estate of the beneficiary.

- Estate Recovery. There is no Medicaid estate recovery against a Self-Settled Special Needs Trust, but a payback provision has the same effect.

- Elective Share. Assets in a Self-Settled Special Needs Trust would be considered subject to the elective share.

Irrevocability

While the above-referenced statutes do not mention irrevocability, the POMS do require that a Self-Settled Special Needs Trust be irrevocable.

Spendthrift Clause

The Social Security Administration requires that a Self Settled Special Needs Trust have a spendthrift clause. The purpose of this clause is to prevent the beneficiary of the trust from assigning trust assets. If the beneficiary had the right to assign the corpus of the trust the assets would be available and the trust would not qualify as a Special Needs Trust. Even though the trust contains a spendthrift provision, it is not immune from claims of the beneficiary’s creditors, unless it is established in a state that has a Domestic Asset Protection Trust statute. A First-Party Special Needs Trust is a Self-Settled Trust and, therefore, subject to claims of creditors. New Jersey does not have a Domestic Asset Protection Trust statute.

1 42 u.s.c. § 13 96p( d ) (4)( A).

2 Draper v. Colvin, DSD Civ. 12-4091-KES Ouly 10, 2013); U.S. Cou rt or Appeals 5th Cir. No. 13-2757 (Mar. 3, 2015).

By Thomas D. Begley, Jr., CELA

One of the trusts used in Medicaid Planning is a Disability Annuity Special Needs Trust (“DASNT”). A previous Straight Word article discussed a Disability Annuity Trust (“DAT”). These trusts are designed so that an individual can establish a trust and transfer assets to the trust for the benefit of a disabled child of any age or a disabled individual under age 65 without incurring a Medicaid transfer of asset penalty. The problem with that trust is that the assets in the trust are considered available for public benefit purposes. Therefore, if a DAT were established for the benefit of an individual receiving Supplemental Security Income (“SSI”) and/or Medicaid, they would become ineligible for those public benefits because the assets in the trust would be countable. The solution would be to wrap a DAT inside a Special Needs Trust (“SNT”). In a Medicaid Planning context, the monies to be used to fund the trust would belong to the third party, usually a parent or a grandparent, so the SNT would be a Third-Party Special Needs Trust (“TPSNT”). In a typical situation, the parent would require long-term care and be applying for Medicaid. In order to become immediately eligible, from an asset standpoint, the parent would transfer the assets to a DASNT. The trust is exempt from the SSI and Medicaid transfer of asset penalties, and the assets in the trust would not be considered available because of the special needs provisions.

Generally, a family member, other than the trust beneficiary, would be the trustee of the DASNT, although a professional trustee could be utilized.

There are seven main issues to be considered in drafting any trust involving a potential Medicaid recipient.

These include:

- Availability;

- Transfer of asset penalty;

- Payback provision;

- Funding;

- Tax considerations, including income, gift and estate taxes;

- Estate recovery; and

- Elective share.

Let’s examine each of these issues in the context of a DASNT.

Availability

The assets in the DASNT would not be available, because the trust would be designed to give the trustee complete discretion with respect to distributions. Standard Third Party Special Needs Trust language would be used in designing the trust. The standard DAT language would also be included. Because of the special needs provisions, the assets in the trust are not counted as assets of the beneficiary.

Transfer of Asset Penalty

There would be no transfer of asset penalty imposed upon the grantor, usually a parent or grandparent, by SSI and Medicaid, because there is a statutory exemption(1) from the penalties for transfers of assets to or for the sole benefit of individuals with disabilities. For a child with a disability, there is no age limit. If the beneficiary of the DASNT is an individual other than a child, there is an age limit of 65.

Payback

Whether a “sole benefit of” trust is subject to a Medicaid payback is open to question. New Jersey takes the position that such a trust must include a Medicaid payback and this issue has not been litigated. Under the provisions of HCFA Transmittal 64, a payback does not appear to be required so long as distributions are made to the beneficiary on an actuarially sound basis. This means that the distributions must be made over the actuarial life expectancy of the beneficiary as determined by the tables contained in HCFA Transmittal 64. Many states follow this interpretation with respect to “sole benefit of” trusts including DATs and DASTs.

Funding

Because a DASNT is a crisis Medicaid planning strategy, generally all assets are placed in the trust. A careful analysis must be made as to whether to include retirement accounts. If the life expectancy of the grantor is short, a better strategy may be to take the risk and use the retirement accounts to pay for care. If the life expectancy is longer, the best strategy may be to simply pay the tax and transfer the after-tax assets to the DASNT.

Tax Considerations

- Income. The income generated by a DASNT is taxed to the beneficiary.

- Gift. There would be a gift from the grantor to the trust for gift tax purposes.

- Estate tax. The assets in the trust would be excluded from the estate of the grantor, but included in the estate of the beneficiary.

Estate Recovery

There would be no Medicaid estate recovery from the estate of the grantor, but there would be estate recovery from the estate of the beneficiary. Since the state requires a payback, then the payback would replace the estate recovery provisions. The payback would include all medical assistance paid to the beneficiary since birth.

Elective Share

Transfers of assets to a DASNT would be subject to elective share considerations. It is good practice for both spouses to contribute the assets to the DASNT.

Comparison Between DAT and DASNT

CONSIDERATION DAT DASNT

Typical Grantor Parent/Grandparent Parent/Grandparent

Typical Trustee Family Member (Non-Beneficiary) Family Member (Non-Beneficiary)

Assets Available Yes No

SSDI/Medicare Yes Yes

SSI/Medicaid No Yes

Transfer Penalty No No

HEMS Standard Yes No

SNT Standard No Yes

(1) 42 U.S.C. §1396p(c )(2)( B).

The post Disability Annuity Special Needs Trusts first appeared on SEONewsWire.net.]]>Consider this example. Your mother created a Revocable Living Trust which divides one share of the trust among her then-living grandchildren, to be held in further trust for their benefit until they reach age 30, when they are entitled to an outright distribution of the remaining assets of their separate trust, and distributions are purely discretionary until age 30. When this trust was created, your daughter, who has Down Syndrome, was not yet born and like most people, your mother didn’t think to update her trust as a result of your daughter’s disability. When your mother dies, your daughter is 28 years old, is receiving SSI, lives in her own apartment that is subsidized by Section 8, and receives in-home support which is provided by a Medicaid waiver – she is happy and you know that your daughter’s current benefits and living arrangements provide a plan for her continued independence upon your death, and the loss of those benefits would jeopardize that plan. Your gut tells you that your daughter’s inheritance could be detrimental so you call Hook Law Center, and we inform you that a distribution of the assets at age 30 would cause your daughter to go over the $2,000 asset limit which would result in your daughter’s ineligibility for public benefits. We also explain that since your daughter is not yet 30, that pursuant to Virginia law, the trustee of the trust may exercise a decanting power by assigning trust principal or income to the trustee of a second trust (without the approval of the court of the beneficiaries) and that this second trust may be a special needs trust to protect your daughter’s public benefit eligibility.

While we have had to decant an old irrevocable trust into a special needs trust on a number of occasions, the question has often been whether this new second trust would be considered by the Social Security Administration and Medicaid offices to be a first-party special needs trust subject to a Medicaid payback, or whether this new trust would be considered a third-party supplemental needs trust. The first notable case pertaining to this issue was In the Matter of the Application of Alan D. Kross (N.Y.Surr.Ct. (Nassau Cty.), No. 2012-369907, Sept. 30, 2013). In that case, Daniel Schreiber was the beneficiary of his grandfather’s trust. Pursuant to the terms of the trust, Daniel was entitled to discretionary distributions of income and principal until age 21. Upon the age of 21, Daniel was entitled to mandatory income distributions paid at least quarterly, half of the principal at age 25, half of the remaining principal at age 30, and the balance of the trust assets at age 35. These mandatory distributions would have disrupted Daniel’s eligibility for SSI and Medicaid, so the trustees filed a petition requesting the court to approve the decanting of trust assets into a new third party supplemental needs trust prior to Daniel’s 21st birthday. The court determined, in addition to other things, that because the old trust was a third party trust, the decanting of the trust assets occurred prior to Daniel’s right to receive the mandatory distributions. Therefore, decanting into the third-party supplemental needs trust was proper, and that no Medicaid payback would be required for the new trust. The New York State Department of Heath appealed the decision, which was upheld by Supreme Court of New York, in Matter of Kroll v. New York State Department of Heath.

The breadth of this case’s impact is not yet known. It may be that this case, only sets a precedent in New York when a beneficiary has not yet obtained the age to receive the outright distribution, or it may extend to all states and in cases where the distribution standards of the trust cause the trust to be an available resource. Regardless of the impact, those of us that focus on helping persons with special needs now have something we can turn to in considering how the decanting of a trust into a special needs trust may be treated in the future.

Ask Kit Kat – Pet Sitters

Ask Kit Kat – Pet Sitters

Hook Law Center: Kit Kat, what should someone look for in the ideal pet sitter?

Kit Kat: Well, there are several things you can consider when deciding to hire a pet sitter. Some need a sitter while they are away at work, and others only require them while they are away on vacation. My parents use a local pet sitting service called Critter Care. They’ve used it for many years going back to the early 1990s. Over the years, we’ve had several caregivers, but all have been excellent. Critter Care screens its employees; they are bonded, so the hard work is done for you. During each caretaking session, the caregiver keeps a daily log of when they arrive and leave your house. They also write observations about how your pet(s) behaved while they were tending to them. As a bonus, they will take in the mail and trash and even water plants that might be in flower pots. Fees are based on the number of pets and number of visits needed. Since we are an all-cat family, once a day is sufficient, but they will come as often as you like. We really like this, because we get to stay in our own house, and do not have to go to the vet and hear dogs barking at all hours of the day and night. We cats find that very off-putting!

Other possible sources for finding pet sitters are through national associations such as the National Association of Pet Sitters (NAPPS) and Pet Sitters International. Or your vet may have some recommendations. Sitters through associations usually have the advantage of being able to read reviews of the possible candidates. Make sure before hiring someone, you actually interview them and see how they interact with your pet. Sometimes your instincts are the best guide. Wendy Pridgen of Boyds, Maryland says, ‘Sometimes you just have to trust your gut and go with what feels right to you.’ And if Ms. Pridgen’s experience is any guide, there will be ups and downs in the process. At first, she hired a college student, and things worked out for a year. Then, the college student became erratic. She used her to take care of her 2 large dogs who needed to be walked during Ms. Pridgen’s long work days. There were signs the student wasn’t coming, so Ms. Pridgen left a broom by the door the student would enter. Ms. Pridgen exited by another door. When she found the broom hadn’t been disturbed, she knew the student wasn’t taking care of her dogs. The student was fired, and she eventually found a new one through a listing on a bulletin board of a local convenience store.

So, be aware that when you hire a pet sitter, it’s like anything else. Sometimes your first efforts will not be successful, but you keep on trying until you find a good fit for both you and your pet. (Ruthanne Johnson, “Someone to watch over them,” All Animals, November/December 2016, p.34-37)

Distribution of This Newsletter

Hook Law Center encourages you to share this newsletter with anyone who is interested in issues pertaining to the elderly, the disabled and their advocates. The information in this newsletter may be copied and distributed, without charge and without permission, but with appropriate citation to Hook Law Center, P.C. If you are interested in a free subscription to the Hook Law Center News, then please telephone us at 757-399-7506, e-mail us at mail@hooklawcenter.com or fax us at 757-397-1267.The post Decanting an Irrevocable Trust to Protect Public Benefit Eligibility first appeared on SEONewsWire.net.]]>

by

Thomas D. Begley, Jr., CELA

Below is a chart comparing an ABLE Account with a Third-Party Special Needs Trust.

|

|

ABLE ACCOUNT |

THIRD PARTY SPECIAL NEEDS |

|

Onset of Disability |

Qualifying

|

No requirement |

|

Age of Beneficiary

|

No requirement |

No requirement |

|

Who May Establish

|

Beneficiary, parent, guardian, agent |

Anyone except beneficiary |

|

Number of Accounts

|

One per beneficiary |

Unlimited |

|

Fees

|

Financial institution fees |

Attorney and trustee fees |

|

Contribution Limits |

$14,000

|

Unlimited |

|

Investment Options |

Investment strategies may be changed twice annually

|

No restrictions |

|

Valid Distributions |

Broadly defined “disability expenses,” including basic living expenses |

Any expenses for sole benefit of beneficiary, with certain implications for

|

|

Taxes |

Earned income is tax-free |

Can use a variety of planning strategies to minimize taxes that may be due. Proper drafting and advice will help

|

|

Medicaid Payback Upon Death of

|

Remaining funds must reimburse state for Medicaid benefits. This is a huge disadvantage for larger accounts. |

No payback |

|

Payments for Food or Shelter Reduce SSI

|

No |

Yes |

The post ABLE ACCOUNT, THIRD PARTY SPECIAL NEEDS TRUST AND POOLED TRUST: COMPARE first appeared on SEONewsWire.net.]]>

by Thomas D. Begley, Jr., CELA

New Jersey has passed the Achieving a Better Life Experience ACT (“ABLE”). While the Act has passed, it will take some time to implement. Many commentators believe that by the end of the year accounts will be authorized.

Under the ABLE Act, people with disabilities and their families may set up special savings accounts similar to 529 Plans to be used for disability-related expenses. Earnings on these accounts are non-taxable. Generally, if the fund does not exceed $100,000, it will not be counted for Supplemental Security Income (“SSI”) purposes. If the fund exceeds $100,000 then SSI will be suspended, but Medicaid can be continued so long as the total amount in the account does not exceed the amount authorized for 529 Plans. To be eligible, an individual must become disabled prior to age 26 and be disabled. If the individual receives Supplemental Security Disability Income (“SSDI”) or SSI or files a Disability Certification under IRS Regulations, she will be considered disabled.

Funds can be used for education, housing, transportation, employment training, support, assistive technology, personal support services, health, prevention and wellness, financial management and administrative fees as well as legal fees and expenses for oversight and monitoring.

The total amount contributed to an ABLE account in any one calendar year by all contributors cannot exceed the amount of the federal annual gift tax exclusion, which for 2016 is $14,000. The drawback to these accounts is on the death of the account owner, any funds remaining in the account must be used to repay Medicaid for any funds advanced on behalf of the account holder. The best strategy seems to be to use these accounts for small gifts. Normally, these accounts would be used for gifts from parents. As long as the gifts are less than $14,000 per year and do not accumulate very much, these accounts might make sense. However, because of the Medicaid payback, it does not make sense to have these accounts grow. A Third Party Special Needs Trust is a much better option, if the amount involved is significant.

The advantages of an ABLE account are the tax-free income. However, realistically this is not a significant advantage because the income on small accounts is low and the other income of the beneficiary with a disability is usually low, so the tax saving sounds more attractive than it actually is. A second advantage is that there is a minimal cost to establishing the account when compared to establishing a Pooled Trust or a Third Party Special Needs Trust. A third advantage is that distributions from an ABLE account for the beneficiary’s food and shelter do not reduce the beneficiary’s SSI payment.

The disadvantages are the Medicaid payback and the possible loss of SSI. Because of the Medicaid payback, it makes little sense to build up a large account. The SSI benefit of approximately $750 per month is a significant benefit that should be protected.

Ideally, ABLE accounts appear to be useful if they are in the $25,000 to $50,000 range, but not for larger accounts. A Pooled Trust or Special Needs Trust would be more appropriate.

The post ABLE ACCOUNTS ARE COMING TO NEW JERSEY first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

Availability. Assets in a Self-Settled Special Needs Trust (“SSSNT”) are not considered available for Supplemental Security Income (“SSI”) or Medicaid eligibility purposes. The reason is that the trustee is given sole discretion with respect to distributions from the trust. The beneficiary cannot control distribution or revoke the trust. Special needs language should be included for guidance to the trustee with respect to distributions.

Transfer of asset penalty. There is no transfer of asset penalty for SSI and Medicaid, because there is a statutory exemption under 42 U.S.C. § 1392b and 42 U.S.C. § 1396p(d)(4)(A).

Payback. A payback to Medicaid is required by law. The payback is for all Medicaid benefits received by the beneficiary since birth. It is not sufficient to pay back Medicaid benefits received from the date of the establishment of the trust to date. In the case of a personal injury settlement, the Medicaid payback is not limited to medical assistance related to the personal injury. All medical assistance provided by Medicaid from birth, whether or not related to the injury, must be included in the payback.

Funding. SSSNTs are generally funded by personal injury recoveries, inheritances, equitable distribution, alimony or child support. However, any asset can be used to fund an SSSNT.

Tax considerations.

- An SSSNT is considered a grantor trust. Therefore, the income earned by the trust is taxed to the beneficiary at the beneficiary’s tax rates.

- Transfers to an SSSNT are not completed gifts.

- Estate tax. Assets in an SSSNT are included in the estate of the beneficiary.

Estate recovery. There is no Medicaid estate recovery against an SSSNT, but a payback provision has the same effect.

Elective share. Assets in an SSSNT would be considered subject to the elective share.

The post SEVEN PLANNING CONSIDERATIONS IN THE CONTEXT OF SELF-SETTLED SPECIAL NEEDS TRUST first appeared on SEONewsWire.net.]]>

by Thomas D. Begley, Jr., CELA

A Third Party Special Needs Trust is usually used in a Medicaid context not for the benefit of the grantor of the trust, but for the beneficiary. The grantor of the trust is typically a parent, but could be grandparent, sibling, other relative or friend. The grantor uses the grantor’s assets to fund the trust. The assets of the beneficiary cannot be used to fund a Third Party Special Needs Trust. In order for the trust to be a Special Needs Trust, the beneficiary must be disabled. Disability is usually determined by the fact that the beneficiary has received a Determination of Disability from the Social Security Administration and is receiving either Supplemental Security Income (“SSI”) or Social Security Disability Income (“SSDI”). The trust is designed so that the assets are not counted for SSI or Medicaid eligibility purposes. The beneficiary is then able to take advantage of the continuation of public benefits including usually SSI and Medicaid, as well as use the assets in the trust to enrich the beneficiary’s life. The trustee is given complete discretion with respect to distributions, and special needs language is used in designing the trust. Provisions made for distributions to the beneficiary during the beneficiary’s lifetime and distribution of any remaining principal and accrued income upon the death of the beneficiary.

The post WHAT IS A THIRD PARTY SPECIAL NEEDS TRUST? first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

There are four main issues to be considered in drafting any trust involving a potential Medicaid recipient. These include:

- Availability;

- Transfer of asset penalty;

- Payback provision; and

- Tax considerations, including income, gift and estate taxes.

Let’s examine each of these issues in the context of a DASNT.

Availability. The assets in the DASNT would not be available, because the trust would be designed to give the trustee complete discretion with respect to distributions. Standard Third-Party Special Needs Trust language would be used in designing the trust. The standard DAT language would also be included. Because of the special needs provisions, the assets in the trust are not counted as assets of the beneficiary.

Transfer of Asset Penalty. There would be no transfer of asset penalty imposed upon the grantor, usually a parent or grandparent, by SSI and Medicaid, because there is a statutory exemption[1] from the penalties for transfers of assets to or for the sole benefit of individuals with disabilities. For a child with a disability, there is no age limit. If the beneficiary of the DASNT is an individual other than a child, there is an age limit of 65.

Payback. Whether a “sole benefit of” trust is subject to a Medicaid payback is open to question. New Jersey takes the position that such a trust must include a Medicaid payback and this issue has not been litigated.

Tax Considerations

- Income. The income generated by a DASNT is taxed to the beneficiary.

- Gift. There would be a gift from the grantor to the trust for gift tax purposes.

- Estate tax. The assets in the trust would be excluded from the estate of the grantor, but included in the estate of the beneficiary.

[1] 42 U.S.C. §1396p(c)(2)(B).

The post CONSIDERATIONS IN DRAFTING A DISABILITY ANNUITY SPECIAL NEEDS TRUST first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

One of the trusts used in Medicaid Planning is a Disability Annuity Special Needs Trust (“DASNT”). A previous article discussed a Disability Annuity Trust (“DAT”). These trusts are designed so that an individual can establish a trust and transfer assets to the trust for the benefit of a disabled child of any age or a disabled individual under age 65 without incurring a Medicaid transfer of asset penalty. The problem with that trust is that the assets in the trust are considered available for public benefit purposes. Therefore, if a DAT were established for the benefit of an individual receiving Supplemental Security Income (“SSI”) and/or Medicaid, they would become ineligible for those public benefits because the assets in the trust would be countable. The solution would be to wrap a DAT inside a Special Needs Trust (“SNT”). In a Medicaid Planning context, the monies to be used to fund the trust would belong to the third party, usually a parent or a grandparent, so the SNT would be a Third-Party Special Needs Trust (“TPSNT”). In a typical situation, the parent would require long-term care and be applying for Medicaid. In order to become immediately eligible, from an asset standpoint, the parent would transfer the assets to a DASNT. The trust is exempt from the SSI and Medicaid transfer of asset penalties, and the assets in the trust would not be considered available because of the special needs provisions.

Generally, a family member, other than the trust beneficiary, would be the trustee of the DASNT, although a professional trustee could be utilized.

The post DISABILITY ANNUITY SPECIAL NEEDS TRUST first appeared on SEONewsWire.net.]]>Moving to another state is a big undertaking for any family, but it can be particularly complicated when a family member has a disability. The secrets to a successful transition are advance planning and a backup plan in case of problems. Here are a few specifics to keep in mind.

Know what to expect with public benefits

If your family member with a disability is receiving Social Security Disability Insurance (SSDI) benefits, there should be no disruption in payments, as long as you inform the Social Security Administration as early as possible of your change of address. Supplemental Security Income (SSI) benefits should not be disrupted either, but the amount could change. In 2016, the federal maximum SSI benefit for an individual is $733 per month. However, some states add an optional state supplement or make food stamps or other benefits available to SSI beneficiaries, so those benefits may vary by state.

Plan in advance for health care needs

Health care is a primary concern, and in this area much can change when moving to another state. In addition to finding new doctors, therapists and other service providers, you should be prepared for changes in coverage. Private health insurance policies may have different coverage or premiums in another state. If you signed up for health insurance through the Affordable Care Act state exchanges, you can take advantage of a 60-day special enrollment period, but be sure to check the eligibility requirements ahead of time. Medicare benefits should not be affected by an interstate move, but Medicaid will need to be reapproved in the new state, and the services and support available through Medicaid varies from state to state.

Special education and other services

While students with disabilities are guaranteed a free and appropriate public education by the federal Individuals with Disabilities Education Act (IDEA), a special needs student’s Individualized Education Program (IEP) will need to be renegotiated. Other services, such as day care, social programs and in-home services vary greatly from state to state. ABLE Act legislation has not yet been enacted in all 50 states, and special needs trusts should be reviewed by an attorney to ensure that they are up to date and there are no problems created by the move.

Moving to a new state is a big project, but creating a checklist and engaging in advance planning will help you have an organized approach. Even with a detailed plan, it is a good idea to have a backup plan, and an emergency fund, in case of pitfalls along the way.

Learn more about our special needs planning and special education advocacy services at www.littmankrooks.com or www.specialneedsnewyork.com.

Was this article of interest to you? If so, please LIKE our Facebook Page by clicking here or sign up for our monthly newsletter.

![]()

by Thomas D. Begley, Jr., CELA

A Disability Annuity Trust (“DAT”) can be established for a disabled child or any disabled individual.[1] However, in considering the use of a DAT for a disabled person, care must be taken to examine the other government benefits currently being received, or which may be received in the future by the person with disabilities.

If the person with disabilities is receiving Supplemental Security Disability Income (“SSDI”), this is usually accompanied by Medicare. SSDI and Medicare are insurance-based programs, rather than means-based programs. Receipt of income from the DAT would not cause a loss of SSDI or Medicare. However, consideration should be given to other benefits that the person with disabilities may receive in the future. For example, will the person with disabilities be a candidate for group housing in the future? If so, the existence of the DAT may cause them to lose that benefit.

If the person is receiving Supplemental Security Income (“SSI”), that person also receives Medicaid. SSI is a means-based program. Both resources and income are considered in determining eligibility. If the person with disabilities receives distributions from the DAT, this may well disqualify that person from receiving SSI and cause a loss of Medicaid. The assets in the DAT would be “available” which would also disqualify the SSI recipient from both SSI and Medicaid, because the assets in the trust would be considered resources. If a DAT is designed as a Special Needs Trust, public benefits may be preserved.

[1] HCFA Transmittal 64 § 3257(B)(6).

The post ESTABLISHING A DISABILITY ANNUITY TRUST FOR A BENEFICIARY RECEIVING SSDI OR SSI first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

Introduction

The United States Supreme Court in a 9-0 unanimous ruling held that an inherited IRA is not protected in bankruptcy under federal law.[1] Heidi Heffron-Clark inherited an IRA from her mother in 2001 and filed for bankruptcy nine years later. The court held that the IRA was not shielded from her creditors, because the funds were not earmarked exclusively for retirement. The Supreme Court indicated that creditor protection does not apply to inherited IRAs for a number of reasons:

- Beneficiaries cannot add money to an inherited IRA like IRA owners can to their accounts;

- Beneficiaries of inherited IRAs must generally begin to make Required Minimum Distributions (RMDs) in the year after they inherit the accounts regardless of how far away they are from retirement;

- Beneficiaries can take total distributions of their inherited accounts at any time and use the funds for any purpose without a penalty. IRA owners must generally wait until age 59-1/2 before they can take penalty-free distributions.

The court held that inherited IRAs do not contain funds dedicated exclusively for use by individuals during retirement. As a result, the favorable bankruptcy protection afforded to retirement funds under the Federal Bankruptcy Code does not apply.

The court did not rule on whether a Spousal Rollover IRA is protected from creditors. Like other IRA owners, if the money is rolled into their own IRA, they may have to pay a 10% early-withdrawal penalty if money is taken before age 59-1/2. If the money is not rolled over into the Spousal Rollover account, then it would appear that the assets will not be protected in bankruptcy.

A way to safeguard IRA and other retirement account assets from creditors is to name a trust as beneficiary of the retirement account.

Trust as Beneficiary

- The best practice is to name a standalone retirement trust as beneficiary for IRAs and other tax-deferred retirement accounts. Naming a trust as beneficiary provides more control. A trust can be drafted to protect the assets from a beneficiary’s creditors.

- If retirement account monies are left directly to heirs, the funds may be squandered by the heirs defeating any benefit of the long-term tax deferral. The trust provides protection from premature withdrawal.

- If the heir is divorced, the retirement account funds may be subject to claims of the non-heir spouse, or if the IRA is in a trust, the non-heir spouse will not be able to attach them.

- Benefit of Beneficiary. If a parent names a child as beneficiary of the parent’s retirement account and subsequently the child dies, that child may name the child’s spouse as beneficiary and the child’s spouse may remarry naming the new spouse as beneficiary. The retirement account would no longer remain in the bloodline. The trust can be designed so that on the death of the child the account passes to other family members and is kept in the bloodline.

- Special Needs. If the beneficiary has special needs, the trust can be drafted to protect the beneficiary’s entitlement to government programs such as SSI, Medicaid or any other means-tested public benefits.

- Finally, if the funds are placed in a trust no guardianship proceeding is needed upon the beneficiary’s incapacity.

[1] Clark v. Rameker, 134 S. Ct. 2242 (2016).

The post RETIREMENT ACCOUNT TRUSTS – PART 1 first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

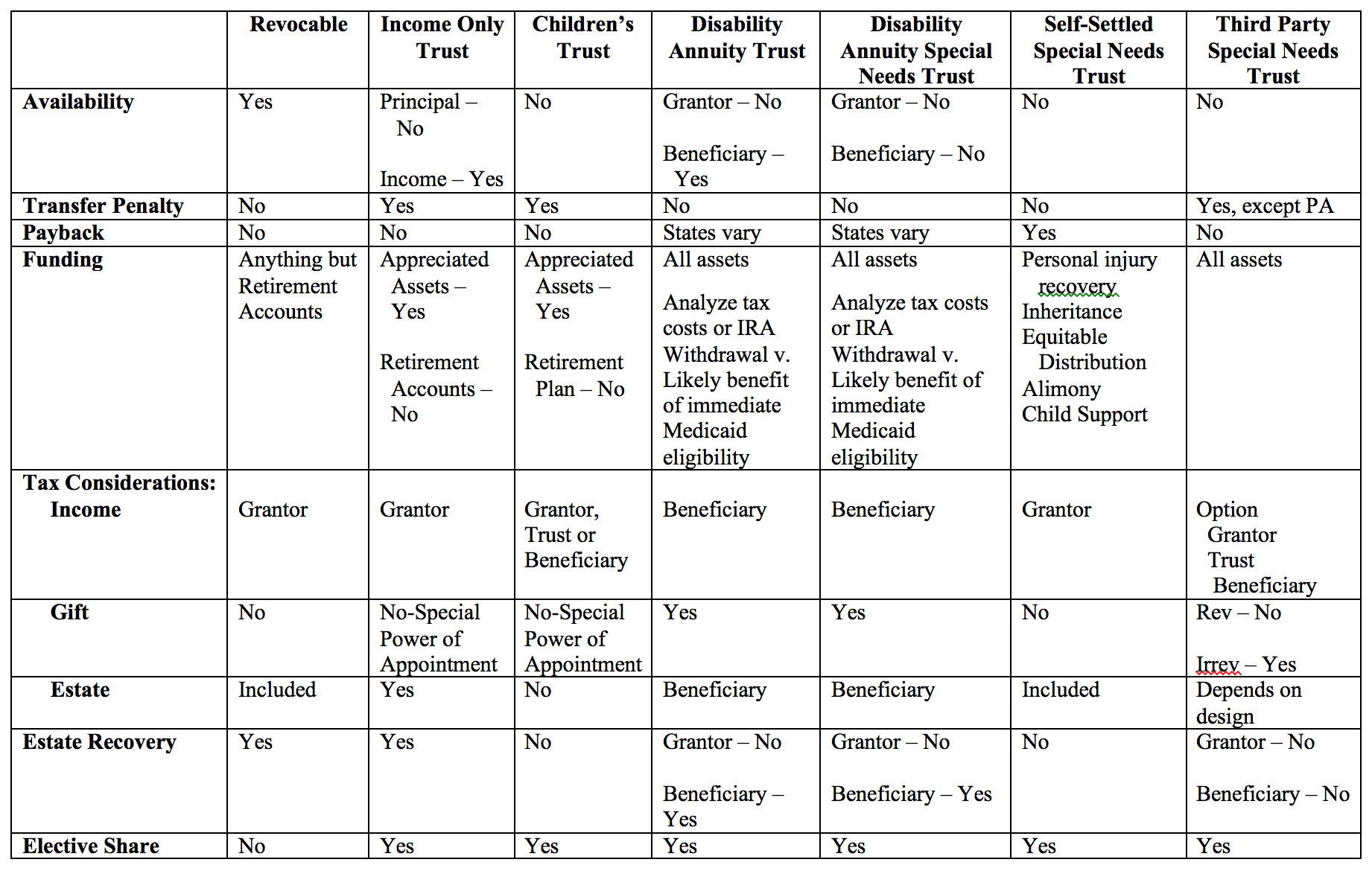

There are seven Trust that should be addressed in considering Medicaid. These are: Revocable Trusts, Income Only Trusts, Children’s Trusts, Disability Annuity Trusts, Disability Annuity Special Needs Trusts, Self-Settled Special Needs Trusts, and Third Party Special Needs Trusts.

There are seven considerations in drafting trusts. These are: availability of trust assets, applicability of a Medicaid or SSI transfer penalty, Medicaid payback provisions, good and bad assets for funding trusts, tax considerations (including income, gift and estate), estate recovery, and elective share issues. This chart is designed to address each of those issues with each of those trusts at a glance.

Having a child who has special needs can take its toll on a marriage. If you find yourself facing divorce and have a child or children who have special needs, there are some areas you will need to focus on working out during the divorce, besides the standard divisions of assets.

Having a child who has special needs can take its toll on a marriage. If you find yourself facing divorce and have a child or children who have special needs, there are some areas you will need to focus on working out during the divorce, besides the standard divisions of assets.

Articulating what you both think your child’s abilities and needs are

The best place to start is to be clear that you both agree on what the child can and cannot do for themselves and the degree of assistance or care they will need. This will cover the additional help needed at home, school or with counselors.

Choosing who the child will live with

Deciding on who gets custody of the child, and whether it will be sole custody or joint custody, are hard decisions to make even with kids who don’t have special needs. When you factor in the unique needs of a special needs child, this decision becomes even more critical to the well being of the child. it will be important to put your child first when you decide on where he or she will stay. For a child with autism for instance, pulling them out of a familiar environment will make an already difficult situation harder. Try and work it out so that the parent who will be responsible for the child stays on in the family home. Don’t shift neighborhoods if you can avoid it, so they continue going to the same school and are not uprooted from a familiar social circle.

Working out a plan for adulthood

With special needs kids, the need for parental support may last well into their adult years. Provisions must be made for the emotional and financial well being of the child and decisions made on what happens once the child becomes an adult. Insurance plans may also be needed to offer them additional protection in the event of the death of the primary caregiving parent.

Alimony, child support, and public benefits

While working out alimony and child support, keep in mind that your child may need financial support even as an adult, in some cases this is a lifelong need. You will also have costs related to additional care, counseling or special medical treatment. However, you may also be eligible for public benefits.

Estate planning

Work through what happens in the event you or your ex pass away. How will the estate be handled? Will there be someone appointed to oversee managing the estate? Work out these details to ensure you secure future for your child who may need to live off their inheritance from you and your ex. Detail what happens should either of you remarry and have kids.

Wherever possible try and consult with a divorce attorney familiar with special needs cases. They will be able to guide you on the role of Medicaid or SSI, special needs trusts and other benefits that apply to your situation, to ensure the best outcome for you, your spouse and your special needs child.

Gerald A. Maggio is an experienced Orange County divorce and family law attorney and family law attorney located in Irvine, California, serving the Orange County and Riverside areas. Mr. Maggio assists clients with legal issues including divorce, legal separation, divorce mediation, child custody, prenuptial agreements, stepparent adoptions, and other family law issues. Mr. Maggio has practiced law in California since 1999, and founded The Maggio Law Firm in 2005, focusing exclusively on divorce and family law matters.

Gerald A. Maggio is an experienced Orange County divorce and family law attorney and family law attorney located in Irvine, California, serving the Orange County and Riverside areas. Mr. Maggio assists clients with legal issues including divorce, legal separation, divorce mediation, child custody, prenuptial agreements, stepparent adoptions, and other family law issues. Mr. Maggio has practiced law in California since 1999, and founded The Maggio Law Firm in 2005, focusing exclusively on divorce and family law matters.

by

Thomas D. Begley, Jr., CELA

Below is a chart comparing an ABLE Account with a Third-Party Special Needs Trust.

|

|

ABLE ACCOUNT |

THIRD PARTY SPECIAL NEEDS |

|

Onset of Disability |

Qualifying to

|

No |

|

Age of Beneficiary

|

No |

No |

|

Who May Establish

|

Beneficiary, |

Anyone |

|

Number of Accounts

|

One |

Unlimited |

|

Fees

|

Financial |

Attorney |

|

Contribution Limits |

$14,000 for SSI total

|

Unlimited |

|

Investment Options |

Investment

|

No |

|

Valid Distributions |

Broadly |

Any

|

|

Taxes |

Earned |

Can

|

|

Medicaid Payback Upon Death of

|

Remaining for Medicaid benefits. |

No |

The post ABLE ACCOUNT, THIRD PARTY SPECIAL NEEDS TRUST AND POOLED TRUST: COMPARE first appeared on SEONewsWire.net.]]>

[An article originally published in the Straight Word, March 2016.]

By Thomas D. Begley, Jr., CELA

A Self-Settled Special Needs Trust is funded with the assets of the individual trust beneficiary. These trusts usually involve funds received as a result of a personal injury, inheritance, alimony, or child support. Under federal law, 1 a SelfSettled Special Needs Trust may be established by a parent, grandparent, guardian or court. In cases involving an adult with capacity court involvement is often unnecessary, so it is convenient to have the trust established by a parent or grandparent. In some states, such as New Jersey, it is possible to establish a “dry trust.” This means that the trust is established but not funded until a later date. In other states, a trust is not established until it is funded with at least a nominal amount of money. These are called “seed trusts.” In a strange but significant case,2 the parents of Stephany Draper sought to establish a selfsettled special needs trust for a personal injury settlement that Stephany was receiving. Under the federal statute, a parent of the trust beneficiary is permitted to establish a self-settled special needs trust but the individual is not. Stephany was a competent adult who had executed a power of attorney appointing her parents as agents. The trust was funded by the personal injury settlement. It should be noted that Stephany’s parents did not use the power of attorney to establish the trust. The Social Security Administration (SSA) held the trust to be invalid. There could be no question but that Stephany is the type of person whom Congress intended to benefit from a self-settled special needs trust. What went wrong?

Generally, under traditional trust rules, a trust does not come into existence until it is first funded. The person who first funds the trust is considered the person who established the trust. However, some states, such as New Jersey, permit the establishment of a “dry” or “empty” trust, while other states require that a trust be seeded to be valid. These are called “seed trusts.”

When the parents established the trust, they made no reference to acting as agents under the power of attorney for Stephany. If they had been acting as agents, they would be acting on Stephany’s behalf and the trust would be invalid, because it would have been established by an individual. What the parents did not do was either recite its status as a dry trust and cite the statutory authority, or treat it as a seed trust and fund it with the parents’ money (i.e., $10). It is not entirely clear that treating the trust as a dry trust would have satisfied SSA. Had the parents paid the $10 into the trust, it is likely SSA would have recognized the trust as a valid trust. It should be noted that at the Hearing before the Administrative Law Judge, the Drapers did not rely on the fact that South Dakota permitted dry trusts.

In the appeal to the Federal District Court, counsel for the plaintiffs further confused the issue by stating that the trust is created by the funder and that the trust was funded by the parents using a power of attorney from Stephany. Under traditional trust doctrine, the person who first funds the trust is the establishor. The problem with plaintiff’s counsel’s argument is that if Stephany’s parents usecl a Power of Attorney from Stephany to fund Stephany’s trust, this would mean that Stephany funded the trust ancf was, therefore, the establisher. The Trial Judge noted that the amount of money placed in the trust was the exact amount of the personal injury settlement. This supported the argument of SSA that since Stephany’s money funded the trust, Stephany was the establisher of the trust and, thus, the trust was invalid. The court never determined whether South Dakota was a dry trust state or a seed trust state. The court found that Stephany’s trust was never an empty trust.

It was funded with Stephany’s money and, therefore, she was the establishor.

The Drapers could have avoided the problem had they funded the trust with $10 of their own money. They may also have avoided the problem if they had recited reliance on the South Dakota trust statute declaring that South Dakota recognizes dry trusts.

In the appeal to the 8111 Circuit, the issue was first funding. Unfortunately, the 8111 Circuit upheld the District Court with the result that Stephany’s trust was determined to be invalid, because it was established by Stephany. Essentially, the court held that the person who first funds the trust is the establishor of the trust.

So where does Draper leave us? At a recent conference at Stetson Law School, Ken Brown and Eric Skidmore, from the Social Security Administration (SSA), indicated that SSA is now taking the position that whoever first funds the trust is the establishor of the trust regardless of whether state law authorizes dry trusts. SSA trust reviewers are looking at trusts to determine if a parent deposited $10 or more of the parent’s money. One way to do this is to send Social Security a trust with a $10 bill attached. A better way would be to open a trust bank account with $10 and deposit that $10 before the personal injury settlement is deposited. It is always best practice in selecting a trustee for a First-Party or Third-Party Special Needs Trust to use a corporate fiduciary rather than an individual. The rules for administering these trusts are extremely complex. SSI and Medicaid rules change constantly, and individuals do not have the time or the expertise to keep up with these changes. Improper administration of a Special Needs Trust will cause SSI and/or Medicaid to declare the trust to be invalid. Failure to open a trust bank account with $10 and deposit that first and then deposit the personal injury settlement, may result in the trust being held to be invalid. This is one more technicality.

Although this raises another issue. If a Special Needs Trust is funded with the assets of a third party, it is a Third-Party Special Needs Trust. If a Special Needs Trust is funded with the assets of the beneficiary of the trust, it is a First-Party or Self-Settled Special Needs Trust. What Social Security is now requiring is a hybrid. The trust would be first funded with the assets of a third party (i.e., the parents) and then funded with the assets of the trust beneficiary; however, the trust would be considered a Self-Settled Special Needs Trust.

The post Parents Establishing a Self-Settled Special Needs Trust For A Child: What Can Go Wrong? first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA