By Thomas D. Begley, Jr., CELA

When a personal injury victim receives a settlement, one of the biggest post-settlement problems is making the money last. If the plaintiff is receiving means-tested public benefits, the monies must be put in a Special Needs Trust. How long do the beneficiary and other family members need that money to last? When the size of the settlement is significant, best practices would dictate that a three-step process be followed:

- Counseling Session. A counseling session should be held with the person with disabilities, the family members, if appropriate, the trustee, the attorney drafting the Special Needs Trust and the Personal Injury attorney, if necessary. At that point. a discussion should be held as to what the immediate needs of the beneficiary arc. Typically these would include a home, a vehicle, a vacation and repayment of debt. During the counseling session a budget should be prepared for the plaintiff’s living expenses going forward. The budget could be broken into three sections: (I) shelter expenses. (2) transportation expenses. and (3) personal expenses. For each item of expense a determination should he made as to whether the expense will be paid by the plaintiff or by the trust. A professional trustee should always be used. At that point. the trustee should prepare a Monte Carlo analysis to determine how long the trust will last. The Monte Carlo analysis is complex, but essentially it is based on trust rates of return and trust distributions. The analysis will determine how long the trust will last based on various rates of distribution. It is helpful if the beneficiary can determine how long the trust should last. If it should last the beneficiary’s lifetime and if the plaintiff is healthy, this will likely be calculated on a life of 90 years. If the plaintiff is unhealthy. the life expectancy will be shorter.

- The Depleting Trust. In most instances the plaintiff will tend to adopt a budget for a lifestyle he or she would like without consideration to how long the trust will last and what will happen when the trust is exhausted. If the professional trustee determines that the trust is beginning to deplete more rapidly than agreed upon, there is a five-step process. These include the following: notification, conversations, planning, documentation and continuous follow up.

- Notification. It is recommended that monthly statements of trust activity be sent to all persons required under state statute. These would include beneficiaries, guardians and generally all non-contingent rcmaindermen. If the trust is depleting, a letter should be sent at least annually, indicating:

- the current market value of the account:

- the amount dispersed over the past 12 months: and

- an estimate as to the time in which the trust will be depicted based 0n projected principal distributions for the coming year.

- The depiction letter should indicate that steps can be taken to extend the lifetime of the trust.

- Conversations. Face-to-face conversations should be held with the beneficiary and interested family members to determine if current budget expenditures can be reduced. If so, what can be reduced immediately and what can be reduced over time? The beneficiary, family and support system must understand that the trust will deplete and the time horizon over which it will deplete. There should be a discussion as to whether a different investment allocation strategy should be employed-either a more aggressive strategy to grow assets or a less aggressive strategy to protect current assets. Finally, there should be a discussion as to whether additional funds will he added to the trust such as payments from Structured Settlement Annuities or additions from family members. If the trust contains depleting assets such as real estate or non-liquid securities, such as LLCs, LPs, oil/gas mineral interests. etc., then there should be a discussion as to whether these assets should be liquidated.

- Planning. What is the plan when the trust is depleted? Will the beneficiary then rely solely on government benefits? Will family and friends contribute to care? Will family and friends fund a Third-Party Special Needs Trust to take the place of the Special Needs Trust? Will the Third Party Special Needs Trust be funded with life insurance or retirement plans? Is the beneficiary in a private pay facility? Does this facility accept Medicaid? What will happen to the beneficiary if the current caregiver dies? If the trust is depleted, final accountings must be filed for the trust.

- Documentation. Trustees should retain documentation of trust administration including:

- Monthly statements.

- Annual depletion letter.

- Other communications such as emails or letters. These communications would include discussions regarding a plan for non-liquid trust assets, beneficiary public benefit programs, discussions among interested parties for extending the trust, a final plan for the beneficiary after the trust ls depleted and final administration needs.

- Continuous Follow Up. During the course of administration of the trust, the trustee must ensure that the right benefits are in place, that living arrangements are made, that assets are sold off as required, that the necessary court approvals are obtained and that all steps related to final administration are taken.

- Notification. It is recommended that monthly statements of trust activity be sent to all persons required under state statute. These would include beneficiaries, guardians and generally all non-contingent rcmaindermen. If the trust is depleting, a letter should be sent at least annually, indicating:

- Basic Principles. The third step in making trust assets last is to understand certain basic principles. Most trustees have a limit on what percentage of trust assets can be spent for the purchase of a home. This generally ranges between 15% and 25%. As a rule of thumb, a trust will last the lifetime of the beneficiary if distributions are limited to approximately 4.5% of trust assets annually.

by Thomas D. Begley, Jr., Esquire, CELA

CMS has released the Medicare and Medicaid numbers for 2017. They are as follows:

Medicaid

- Income Cap[1] $2,205

- Maximum Community Spouse Resource Allowance (CSRA)[2] $120,900

- Minimum CSRA[3] $24,180

- Maximum Minimum Monthly Maintenance Needs Allowance (MMMNA)[4] $3,022.50

- MMMNA (July 1, 2016 until June 30, 2017)[5] $2,002.50

- MMMNA (July 1, 2017 until June 30, 2018)[6] $2,030.00

- Excess Shelter Allowance (July 1, 2016 until June 30, 2017)[7] $600.75

- Excess Shelter Allowance (July 1, 2017 until June 30, 2018)[8] $609.00

- Maximum Resource Limit (Individual)[9] $2,000

- Minimum and Maximum Cap on Equity in the Home[10] $560,000 – $840,000

Medicare

Part A

- Medicare Co-Payment – Skilled Nursing Facility (SNF)[11] $164.50

- Hospital Deductible[12] $1,316

- Per day Co-Insurance – Day 61 -90[13] $329

- Per day Co Insurance – Day 91-150[14] $658

Part A Premium (for voluntary enrollees only)

- With 30-39 quarters of Social Security coverage[15] $227

- With 29 or fewer quarters of Social Security coverage[16] $413

Part B

Medicare Part B – Single or Married and Filing Joint Return

Part B Income-Related Premium[19]

| Beneficiaries who file an individual tax return with income:

|

Beneficiaries who file a joint tax return with income: | Income-related monthly adjustment amount | Total monthly premium amount

|

| Less than or equal to $85,000

|

Less than or equal

to $170,000 |

$0.00 | $134.00 |

| Greater than

$85,000 and less than or equal to $107,000

|

Greater than $170,000 and less than or equal to $214,000 | $53.50 | $187.50 |

| Greater than $107,000 and less than or equal to $160,000

|

Greater than $214,000 and less than or equal to $320,000 | $133.90 | $257.90 |

| Greater than $160,000 and less than or equal to $214,000

|

Greater than $320,000 and less than or equal to $428,000 | $214.30 | $348.30 |

| Greater than $214,000 | Greater than $428,000 | $294.60 | $428.50 |

In addition, the monthly premium rates to be paid by beneficiaries who are married, but file a separate return from their spouse and lived with their spouse at some time during the taxable year are:

| Beneficiaries who are married but file a separate tax return from their spouse:

|

Income-related monthly adjustment amount | Total monthly premium amount |

| Less than or equal to

$85,000

|

$0.00 | $134.00 |

| Greater than $85,000 and

less than or equal to $129,000

|

$214.30 | $348.30 |

| Greater than $129,000 | $294.60 | $428.60 |

Standard Part D Cost-Sharing for 2017[20]

- Annual Deductible Maximum $400

- Member Pays 25% of the Next… $3,300 (25% = $825)

- Initial Benefit Period Maximum $3,700 ($400 + $3,300)

- Donut Hole Threshold $3,725

(Brand name drugs: 50% + 10% plan “subsidy,” Generic drug: 49% subsidy)

- Catastrophic Coverage $4,950 ($400 + $825 + $3,725)

- Catastrophic cost-sharing: Generic $3.30/$8.25 or 5% (whichever is greater)

- Catastrophic cost-sharing: Brand $7.40 or 5% (whichever is greater)

[1] 42 U.S.C. §1396a(a)(10)(A)(v); 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[2] 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[3] 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[4] 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[5] 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[6] 82 Fed. Reg. 8832 (Jan. 31, 2017).

[7] 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[8] 82 Fed. Reg. 8832 (Jan. 31, 2017).

[9] 20 CFR § 416.1205(c).

[10] 42 U.S.C. §1396p(f); 2017 SSI and Spousal Impoverishment Standards, www.medicaid.gov.

[11] 81 Fed. Reg. 80062 (Nov 15, 2016).

[12] 81 Fed. Reg. 80062 (Nov 15, 2016).

[13] 81 Fed. Reg. 80062 (Nov 15, 2016).

[14] 81 Fed. Reg. 80062 (Nov 15, 2016).

[15] 81 Fed. Reg. 80072 (Nov 15, 2016).

[16] 81 Fed. Reg. 80071 (Nov 15, 2016).

[17] 81 Fed. Reg. 80063 (Nov 15, 2016).

[18] 81 Fed. Reg. 80063 (Nov 15, 2016).

[19] 81 Fed. Reg. 80066 (Nov 15, 2016).

[20] http://www.medicareadvocacy.org.

The post MEDICAID AND MEDICARE 2017 COLA NUMBERS first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

There are a number of alternatives to a Third Party Special Needs Trusts. These include the following:

- Disinherit a Child. The problem with this strategy is that one cannot be certain that public benefits, as we know them today, will continue forever. Many public benefits have been cut back in recent years and there is no guarantee that current benefits will not be reduced as well. Many parents who have severely disabled children, whose needs are covered by public benefits, will consider disinheriting the children, but they should be made aware that current public benefits may not be there when the child needs them in the future.

- Leave Money to the Child. The problem with this approach is that unless the funds being left to the child are very significant, they may not last long if the child’s needs, particularly medical needs, are great. It is usually better to maintain public benefits and establish a trust for needs or wants that will not be covered by public benefits.

- Leave Funds to Sibling. This is the common strategy that frequently backfires. The idea is to leave the share of the person with disabilities to a brother or sister with the understanding that the brother or sister will use that money to care for the child with disabilities. The problems occur when the child to whom the funds are left is sued by a creditor, is divorced, or simply says, “I want to use this money for myself, not in the Will says that I have to use it for my sibling with disability and I am not going to use for that purpose.” Sometimes it is the sibling that makes this decision, but frequently it is the spouse of the sibling who pushes for that result.

- Pooled Trust. A Pooled Trust is a good solution for relatively small amounts of money. If the trust is less than $100,000, Pooled Trust makes sense. If it is between $100,000 and $200,000, a Pooled Trust should be compared to a Third Party Special Needs Trust. If the amount involved is in excess of $200,000, a Third Party Special Needs Trust is almost always the best solution.

- ABLE Account. New Jersey has adopted legislation authorizing ABLE accounts. These accounts are expected to come into existence sometime in the Fall. A problem is that not more than the gift tax annual exclusion amount can be contributed to an account in any one year and no beneficiary can have more than one account. The annual exclusion gift tax exemption for 2016 is $14,000. So, if the inheritance is $14,000 or less, an ABLE account might make sense.

by

Thomas D. Begley, Jr., CELA

Below is a chart comparing an ABLE Account with a Third-Party Special Needs Trust.

|

|

ABLE ACCOUNT |

THIRD PARTY SPECIAL NEEDS |

|

Onset of Disability |

Qualifying

|

No requirement |

|

Age of Beneficiary

|

No requirement |

No requirement |

|

Who May Establish

|

Beneficiary, parent, guardian, agent |

Anyone except beneficiary |

|

Number of Accounts

|

One per beneficiary |

Unlimited |

|

Fees

|

Financial institution fees |

Attorney and trustee fees |

|

Contribution Limits |

$14,000

|

Unlimited |

|

Investment Options |

Investment strategies may be changed twice annually

|

No restrictions |

|

Valid Distributions |

Broadly defined “disability expenses,” including basic living expenses |

Any expenses for sole benefit of beneficiary, with certain implications for

|

|

Taxes |

Earned income is tax-free |

Can use a variety of planning strategies to minimize taxes that may be due. Proper drafting and advice will help

|

|

Medicaid Payback Upon Death of

|

Remaining funds must reimburse state for Medicaid benefits. This is a huge disadvantage for larger accounts. |

No payback |

|

Payments for Food or Shelter Reduce SSI

|

No |

Yes |

The post ABLE ACCOUNT, THIRD PARTY SPECIAL NEEDS TRUST AND POOLED TRUST: COMPARE first appeared on SEONewsWire.net.]]>

by Thomas D. Begley, Jr., CELA

New Jersey has passed the Achieving a Better Life Experience ACT (“ABLE”). While the Act has passed, it will take some time to implement. Many commentators believe that by the end of the year accounts will be authorized.

Under the ABLE Act, people with disabilities and their families may set up special savings accounts similar to 529 Plans to be used for disability-related expenses. Earnings on these accounts are non-taxable. Generally, if the fund does not exceed $100,000, it will not be counted for Supplemental Security Income (“SSI”) purposes. If the fund exceeds $100,000 then SSI will be suspended, but Medicaid can be continued so long as the total amount in the account does not exceed the amount authorized for 529 Plans. To be eligible, an individual must become disabled prior to age 26 and be disabled. If the individual receives Supplemental Security Disability Income (“SSDI”) or SSI or files a Disability Certification under IRS Regulations, she will be considered disabled.

Funds can be used for education, housing, transportation, employment training, support, assistive technology, personal support services, health, prevention and wellness, financial management and administrative fees as well as legal fees and expenses for oversight and monitoring.

The total amount contributed to an ABLE account in any one calendar year by all contributors cannot exceed the amount of the federal annual gift tax exclusion, which for 2016 is $14,000. The drawback to these accounts is on the death of the account owner, any funds remaining in the account must be used to repay Medicaid for any funds advanced on behalf of the account holder. The best strategy seems to be to use these accounts for small gifts. Normally, these accounts would be used for gifts from parents. As long as the gifts are less than $14,000 per year and do not accumulate very much, these accounts might make sense. However, because of the Medicaid payback, it does not make sense to have these accounts grow. A Third Party Special Needs Trust is a much better option, if the amount involved is significant.

The advantages of an ABLE account are the tax-free income. However, realistically this is not a significant advantage because the income on small accounts is low and the other income of the beneficiary with a disability is usually low, so the tax saving sounds more attractive than it actually is. A second advantage is that there is a minimal cost to establishing the account when compared to establishing a Pooled Trust or a Third Party Special Needs Trust. A third advantage is that distributions from an ABLE account for the beneficiary’s food and shelter do not reduce the beneficiary’s SSI payment.

The disadvantages are the Medicaid payback and the possible loss of SSI. Because of the Medicaid payback, it makes little sense to build up a large account. The SSI benefit of approximately $750 per month is a significant benefit that should be protected.

Ideally, ABLE accounts appear to be useful if they are in the $25,000 to $50,000 range, but not for larger accounts. A Pooled Trust or Special Needs Trust would be more appropriate.

The post ABLE ACCOUNTS ARE COMING TO NEW JERSEY first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

Availability. Assets in a Self-Settled Special Needs Trust (“SSSNT”) are not considered available for Supplemental Security Income (“SSI”) or Medicaid eligibility purposes. The reason is that the trustee is given sole discretion with respect to distributions from the trust. The beneficiary cannot control distribution or revoke the trust. Special needs language should be included for guidance to the trustee with respect to distributions.

Transfer of asset penalty. There is no transfer of asset penalty for SSI and Medicaid, because there is a statutory exemption under 42 U.S.C. § 1392b and 42 U.S.C. § 1396p(d)(4)(A).

Payback. A payback to Medicaid is required by law. The payback is for all Medicaid benefits received by the beneficiary since birth. It is not sufficient to pay back Medicaid benefits received from the date of the establishment of the trust to date. In the case of a personal injury settlement, the Medicaid payback is not limited to medical assistance related to the personal injury. All medical assistance provided by Medicaid from birth, whether or not related to the injury, must be included in the payback.

Funding. SSSNTs are generally funded by personal injury recoveries, inheritances, equitable distribution, alimony or child support. However, any asset can be used to fund an SSSNT.

Tax considerations.

- An SSSNT is considered a grantor trust. Therefore, the income earned by the trust is taxed to the beneficiary at the beneficiary’s tax rates.

- Transfers to an SSSNT are not completed gifts.

- Estate tax. Assets in an SSSNT are included in the estate of the beneficiary.

Estate recovery. There is no Medicaid estate recovery against an SSSNT, but a payback provision has the same effect.

Elective share. Assets in an SSSNT would be considered subject to the elective share.

The post SEVEN PLANNING CONSIDERATIONS IN THE CONTEXT OF SELF-SETTLED SPECIAL NEEDS TRUST first appeared on SEONewsWire.net.]]>

by Thomas D. Begley, Jr., CELA

Trusts for disabled individuals who have not reached age 65 and are funded with assets of the disabled person are authorized under OBRA-93.[1] The trust is for the benefit of disabled persons. The person must be under 65 at the inception of the trust. While the trust must be established and funded prior to the beneficiary attaining the age of 65, it may continue after 65. If the trust is funded with a structured settlement prior to the beneficiary attaining the age of 65, the trust remains viable even though payments from the annuity are received after age 65.

The trusts must be established by a parent, grandparent, legal guardian, or court.

Transfers to the trust are not subject to the transfer of assets rules. The trust should be drafted so that the resources are unavailable. This means that the trustee must have sole discretion with respect to distributions, and the beneficiary must not have any right to revoke the trust. The trust should be administered in such a way that the income is not counted as income to the beneficiary. Distributions can be made to third parties for the sole benefit of the beneficiary, or the beneficiary or a family member can obtain a credit card and send the bill to the trustee for payment so long as the charges on the credit card were for the sole benefit of the trust beneficiary.

The trust must provide that on death the funds remaining in the trust go first to reimburse Medicaid and then for the benefit of other beneficiaries.

[1] 42 U.S.C. § 1396p(d)(4)(A).

The post WHAT IS A SELF-SETTLED SPECIAL NEEDS TRUST? first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

A Third Party Special Needs Trust is usually used in a Medicaid context not for the benefit of the grantor of the trust, but for the beneficiary. The grantor of the trust is typically a parent, but could be grandparent, sibling, other relative or friend. The grantor uses the grantor’s assets to fund the trust. The assets of the beneficiary cannot be used to fund a Third Party Special Needs Trust. In order for the trust to be a Special Needs Trust, the beneficiary must be disabled. Disability is usually determined by the fact that the beneficiary has received a Determination of Disability from the Social Security Administration and is receiving either Supplemental Security Income (“SSI”) or Social Security Disability Income (“SSDI”). The trust is designed so that the assets are not counted for SSI or Medicaid eligibility purposes. The beneficiary is then able to take advantage of the continuation of public benefits including usually SSI and Medicaid, as well as use the assets in the trust to enrich the beneficiary’s life. The trustee is given complete discretion with respect to distributions, and special needs language is used in designing the trust. Provisions made for distributions to the beneficiary during the beneficiary’s lifetime and distribution of any remaining principal and accrued income upon the death of the beneficiary.

The post WHAT IS A THIRD PARTY SPECIAL NEEDS TRUST? first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

The chart below is a brief comparison between a Disability Annuity Trust (“DAT”) and a Disability Annuity Special Needs Trust (“DASNT”).

| Consideration | DAT | DASNT |

| Typical Grantor | Parent/Grandparent | Parent/Grandparent |

| Typical Trustee | Family Member

(Non-Beneficiary) |

Family Member

(Non-Beneficiary) |

| Assets Available | Yes | No |

| SSDI/ Medicare | Yes | Yes |

| SSI/Medicaid | No | Yes |

| Transfer Penalty | No | No |

| HEMS Standard | Yes | No |

| SNT Standard | No | Yes |

The post COMPARISON BETWEEN A DISABILITY ANNUITY TRUST AND A DISABILITY ANNUITY SPECIAL NEEDS TRUST first appeared on SEONewsWire.net.]]>

by Thomas D. Begley, Jr., CELA

There are four main issues to be considered in drafting any trust involving a potential Medicaid recipient. These include:

- Availability;

- Transfer of asset penalty;

- Payback provision; and

- Tax considerations, including income, gift and estate taxes.

Let’s examine each of these issues in the context of a DASNT.

Availability. The assets in the DASNT would not be available, because the trust would be designed to give the trustee complete discretion with respect to distributions. Standard Third-Party Special Needs Trust language would be used in designing the trust. The standard DAT language would also be included. Because of the special needs provisions, the assets in the trust are not counted as assets of the beneficiary.

Transfer of Asset Penalty. There would be no transfer of asset penalty imposed upon the grantor, usually a parent or grandparent, by SSI and Medicaid, because there is a statutory exemption[1] from the penalties for transfers of assets to or for the sole benefit of individuals with disabilities. For a child with a disability, there is no age limit. If the beneficiary of the DASNT is an individual other than a child, there is an age limit of 65.

Payback. Whether a “sole benefit of” trust is subject to a Medicaid payback is open to question. New Jersey takes the position that such a trust must include a Medicaid payback and this issue has not been litigated.

Tax Considerations

- Income. The income generated by a DASNT is taxed to the beneficiary.

- Gift. There would be a gift from the grantor to the trust for gift tax purposes.

- Estate tax. The assets in the trust would be excluded from the estate of the grantor, but included in the estate of the beneficiary.

[1] 42 U.S.C. §1396p(c)(2)(B).

The post CONSIDERATIONS IN DRAFTING A DISABILITY ANNUITY SPECIAL NEEDS TRUST first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

One of the trusts used in Medicaid Planning is a Disability Annuity Special Needs Trust (“DASNT”). A previous article discussed a Disability Annuity Trust (“DAT”). These trusts are designed so that an individual can establish a trust and transfer assets to the trust for the benefit of a disabled child of any age or a disabled individual under age 65 without incurring a Medicaid transfer of asset penalty. The problem with that trust is that the assets in the trust are considered available for public benefit purposes. Therefore, if a DAT were established for the benefit of an individual receiving Supplemental Security Income (“SSI”) and/or Medicaid, they would become ineligible for those public benefits because the assets in the trust would be countable. The solution would be to wrap a DAT inside a Special Needs Trust (“SNT”). In a Medicaid Planning context, the monies to be used to fund the trust would belong to the third party, usually a parent or a grandparent, so the SNT would be a Third-Party Special Needs Trust (“TPSNT”). In a typical situation, the parent would require long-term care and be applying for Medicaid. In order to become immediately eligible, from an asset standpoint, the parent would transfer the assets to a DASNT. The trust is exempt from the SSI and Medicaid transfer of asset penalties, and the assets in the trust would not be considered available because of the special needs provisions.

Generally, a family member, other than the trust beneficiary, would be the trustee of the DASNT, although a professional trustee could be utilized.

The post DISABILITY ANNUITY SPECIAL NEEDS TRUST first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

A Disability Annuity Trust (“DAT”) can be established for a disabled child or any disabled individual.[1] However, in considering the use of a DAT for a disabled person, care must be taken to examine the other government benefits currently being received, or which may be received in the future by the person with disabilities.

If the person with disabilities is receiving Supplemental Security Disability Income (“SSDI”), this is usually accompanied by Medicare. SSDI and Medicare are insurance-based programs, rather than means-based programs. Receipt of income from the DAT would not cause a loss of SSDI or Medicare. However, consideration should be given to other benefits that the person with disabilities may receive in the future. For example, will the person with disabilities be a candidate for group housing in the future? If so, the existence of the DAT may cause them to lose that benefit.

If the person is receiving Supplemental Security Income (“SSI”), that person also receives Medicaid. SSI is a means-based program. Both resources and income are considered in determining eligibility. If the person with disabilities receives distributions from the DAT, this may well disqualify that person from receiving SSI and cause a loss of Medicaid. The assets in the DAT would be “available” which would also disqualify the SSI recipient from both SSI and Medicaid, because the assets in the trust would be considered resources. If a DAT is designed as a Special Needs Trust, public benefits may be preserved.

[1] HCFA Transmittal 64 § 3257(B)(6).

The post ESTABLISHING A DISABILITY ANNUITY TRUST FOR A BENEFICIARY RECEIVING SSDI OR SSI first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

The key issue concerning trusts “for the sole benefit of” is availability. In a private letter, HCFA, now CMS, has taken the position that a trust established for the sole benefit of a community spouse under HCFA Transmittal 64 is an available resource.[1] HCFA maintained that there is a material difference between a standard annuity and an “annuitized” trust. HCFA states:

a standard annuity can protect the funds used to purchase the annuity from being counted as resources in determining eligibility for Medicaid. However, there is a fundamental difference between a standard annuity and the “annuitized” trust you established. A standard annuity requires the actual purchase of a commodity; i.e., the annuity itself. A specific amount of money is given to the entity selling the annuity, in return for which the entity contractually agrees to provide an income stream for a specified period of time. Upon completion of the transaction, the buyer no longer owns the funds used to purchase the annuity. Instead, the buyer owns the annuity itself. If the annuity is irrevocable, as most annuities are, the buyer cannot reclaim ownership of the funds used to purchase the annuity. The buyer is only entitled to the income stream purchased and only for as long as the annuity stipulates. This is essentially the same as the purchase of any item or product where funds are exchanged for ownership of something else.

It is important to note that the letter from HCFA is not law or policy. It is an interpretation of policy as articulated in HCFA Transmittal 64. Under this letter, only the amount of the CSRA could be able to be placed in a “sole benefit of” trust. HCFA Transmittal 64 clearly compares the transfer of assets to a community spouse with the transfer of assets to a trust for the sole benefit of a community spouse.[2] The document clearly states “when transfers between spouses are involved, the unlimited transfer exception should have little effect on the eligibility determination, primarily because resources belonging to both spouses are combined in determining eligibility for the institutionalized spouse.” Thus, resources transferred to a community spouse are still be considered available to the institutionalized spouse for eligibility purposes.

[1] Letter dated April 16, 1998, from Robert A. Streimer, Disabled and Elderly Health Programs Group, Center for Medicaid and State Operations, Health Care Financing Administration, to Jean Galloway Ball.

[2] HCFA Transmittal 64 § 3258.11.

The post WHAT DOES “SOLE BENEFIT OF” MEAN WITH RESPECT TO A DISABILITY ANNUITY TRUST first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

The Concept. A sole benefit of trust is a creature of HCFA Transmittal 64.[1] These trusts have traditionally been used in crisis planning. They can be established for the benefit of disabled persons—a Disability Annuity Trust (“DAT”).[2] The idea is that assets would be transferred to an irrevocable trust for the sole benefit of the disabled individual. The assets in the trust were then paid out to the beneficiary on an actuarially sound basis using the actuarial tables contained in HCFA Transmittal 64.[3] However, some states, including New Jersey, maintain that despite the clear language in HCFA Transmittal 64, the language in the statute “sole benefit of” means that a Medicaid payback provision is required. Because the assets were transferred to an irrevocable trust “for the sole benefit of” a disabled individual, the transfer is not subject to the Medicaid transfer penalty rules.

This is a particularly useful device where (1) there are highly appreciated assets and utilization of the trust makes it possible for a “step up” in basis to be obtained, and (2) advanced planning has not been done and the transfer of assets to children would result in significant periods of Medicaid ineligibility. There are two issues to be considered in utilizing “for the sole benefit of” trusts: transfer rules and availability.

Transfer of Asset Penalty. A sole benefit of trust is exempt from the Medicaid transfer of asset penalties. If the sole benefit of trust is established for a disabled child, there is no age limit.

Age Limit.

- Sole benefit of disabled child. The trust can be established for a disabled child age 65 or older.[4]

- Sole benefit of other disabled individual. If the sole benefit of trust is established for an individual other than a child, the other individual must be under age 65 years of age and disabled.[5]

Definition of sole benefit of. HCFA Transmittal 64 deals with transfers of assets and treatment of trusts.[6] For the sole benefit of is defined as follows:

A transfer is considered to be for the sole benefit of a spouse, blind or disabled child, or a disabled individual if the transfer is arranged in such a way that no individual or entity except for the spouse, blind or disabled child, or disabled individual can benefit from the assets transferred in any way, whether at the time of the transfer or at any time in the future. For a transfer or trust to be considered for the sole benefit of one of these individuals, the instrument or document must provide for the spending of funds involved for the benefit of the individual on a basis that is actuarially sound based on the life expectancy of the individual involved.[7]

Despite the clear definition of sole benefit of in HCFA Transmittal 64, many states, including New Jersey, require that the sole benefit of trust have a provision requiring a payback on the death of the beneficiary to the state Medicaid agency.

Therefore, if the beneficiary is receiving Social Security Disability Income (“SSDI”) and Medicare, a DAT is appropriate. Beneficiaries receiving Supplemental Security Income (“SSI”) and Medicaid must utilize a Disability Annuity Special Needs Trust.

[1] HCFA Transmittal 64 § 3257.

[2] HCFA Transmittal 64 § 3258.9B.

[3] HCFA Transmittal 64 § 3258.9B.

[4] 42 U.S.C. § l396p(c)(2)(B)(iii).

[5] 42 U.S.C. § l396p(c)(2)(B)(iv).

[6] HCFA Transmittal 64 § 3257.

[7] HCFA Transmittal 64 § 3257(B)(6).

The post DISABILITY ANNUITY TRUSTS first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

Funding

Many clients who use Children’s Trusts as part of their Medicaid planning are non-crisis planning clients. They either have an early diagnosis or are elderly but in good health. They are doing advance planning and want a sense of independence. They do not want all of their assets in a trust. Good practice dictates that the lawyer have a discussion with the client and determine how much the client feels should be kept out of the trust to give the client a feeling of comfort. The client should understand that the funds retained outside the trust are at risk, unless they are transferred to children to be held pursuant to the terms of a Family Agreement. Ideally, the trust will be funded with the least amount of assets possible. In calculating how much to put in the trust, the client can carve out assets that can be used in the future for the following:

- Amount of Community Spouse Resource Allowance (CSRA);

- Amount of the anticipated spend down as set forth in the client’s Asset Protection Plan;

- Key money to gain admission to a facility; or

- Any amount of money the client is willing to lose. Typically, a single client will want to retain $50,000 – $100,000 of assets and risk losing that amount in order to preserve a sense of independence. To a certain extent, this will be determined by the medical condition of the client.

Ideal Assets

Ideal assets to fund a Children’s Trust would include appreciated real estate, such as a primary residence or a vacation home, or appreciated securities. There are significant tax advantages in utilizing trusts for these assets as opposed to transferring outright to children. Careful consideration must be given to rental real estate, because the parent would no longer be entitled to the rent after the property is transferred to the Children’s Trust.

Bad Assets

Bad assets to use in funding trusts include retirement accounts, deferred annuities, and government bonds with significant accumulated interest. The problem is the transfer of those assets would result in immediate income tax. To the extent possible, these assets should be left outside the trust.

Tax Considerations

Income Tax

A Children’s Trust can be designed as a grantor trust so that the grantor pays the tax on any income, or .a non-grantor trust where the income is taxed either to the trust itself or to the beneficiary, depending on the design of the trust.

Gift Tax

A Children’s Trust can be designed so that the Grantor retains a limited power of appointment over the trust corpus. The limited power of appointment would enable the Grantor to appoint the remainder of the trust to a limited class of people. Limited power of appointment could be either testamentary or inter vivos.

Estate Tax

If the trust is designed as a grantor trust, then the assets in the trust will be included in the estate of the grantor for estate tax purposes. The Children’s Trust can be designed so that it is not a grantor trust and the assets in the trust would be excluded from the estate of the grantor for estate tax purposes. In determining how to draft the trust, the capital gain tax saving resulting from a step-up in basis must be weighed against any estate tax savings. Usually, payment of the New Jersey estate tax is the lesser of the two evils.

The post FUNDING AND TAX CONSIDERATIONS INVOLVING CHILDREN’S TRUSTS IN MEDICAID PLANNING first appeared on SEONewsWire.net.]]>

by Thomas D. Begley, Jr., CELA

A common Medicaid Planning strategy is to transfer assets to third parties, wait for the five-year lookback to expire and apply for Medicaid. If assets are transferred to children, there are certain risks to be considered. If the child is sued by a creditor, the assets transferred by the parent to the child are subject to the claims of the creditors. If the child is subsequently divorced, the son or daughter-in-law may be able to claim additional funds by virtue of the assets that were transferred by the parent to the child. Basic divorce law says that so long as the transferred funds were not co-mingled by the child and the child’s spouse they are not subject to claims for equitable distribution, but Family Law practitioners all advise that the judge will figure out something else to give the son or daughter-in-law and advise against this strategy. If the child to whom the assets are transferred dies, the parent’s assets can be left by the child’s Will to the child’s spouse or, absent a Will, the child’s spouse will normally inherit by intestacy.

An alternative would be to transfer assets to a Children’s Trust. Under the Children’s Trust, one or more of the children could serve as trustee. The parent would give up all access to the principal being transferred to the trust and any income earned by that principal. The trust could provide that distributions could be made to a child from the principal and/or income. After five years, the assets transferred to the trust would be out of the parent’s name and would not be counted for Medicaid eligibility purposes.

Ideal assets to fund a Children’s Trust are depreciated assets. A primary residence may be the best choice for funding the trust. A second home is also a good choice, particularly if it has appreciated in value.

Retirement accounts are never a good asset to fund a Children’s Trust, because the income tax on the retirement account would have to be paid when the funds are withdrawn to fund the trust.

The post CHILDREN’S TRUSTS first appeared on SEONewsWire.net.]]>

by Thomas D. Begley, Jr., CELA

The following chart compares the advantages and disadvantages of an outright transfer of assets and putting assets in an Income Only Trust.

| Trusts v. Transfers Comparison | ||||

| Issue | Income Only Trusts | Children | ||

| Look-Back | 5 Years | 5 Years | ||

| Control | None | None | ||

| Risk Avoidance | Yes | No | ||

| Estate Recovery | Maybe | No | ||

| Income Tax | Parent | Children | ||

| Gift Tax | Maybe | Yes | ||

| Step Up in Basis | Yes | No | ||

| Principal Residence Exclus. | Yes | No | ||

The post COMPARISON BETWEEN TRANSFERS TO INCOME ONLY TRUSTS AND TRANSFERS TO CHILDREN first appeared on SEONewsWire.net.]]>

by Thomas D. Begley, Jr., CELA

An Income Only Trust can be designed as a grantor trust. The trust assets are unavailable for Medicaid, but there are some potentially significant tax benefits to the grantor. The Internal Revenue Code contains certain requirements for a grantor trust.[1]

Income Tax. Income is taxed at the grantor’s individual tax rate, which is usually less than the trust’s compressed tax rate.

Capital Gains Tax. Capital gains tax treatment is maintained. This is particularly important if the trust is funded with a primary residence. The §121 exclusion from capital gains tax can be maintained. The trust must contain a provision that the trustee must allocate the gain on the sale of the home to principal and not to income.

The benefit of the capital gains tax can be achieved for non-home appreciated assets as well.

Gift Tax. An Income Only Trust can be designed in such a way that a transfer into a trust can be either a gift or not a gift. If the grantor desires that the transfer be considered a gift for tax purposes, a gift tax return would be filed based on the present value of the gift. This would be the value of the assets transferred, less the value of the grantor’s retained interest in the income stream.

Estate Tax. Since the trust is a grantor trust, the entire value of the estate would be included in the grantor’s estate for federal estate tax purposes.[2]

Because the assets are included in the estate of the grantor, the estate should receive a step up in tax basis as to trust assets to the fair market value of the assets as of the grantor’s death. To achieve the step up in basis, the trust should contain a limited power of appointment on death. In many cases, this is a significant advantage over outright transfers to children.

Estate Recovery. The assets in the Income Only Trust would not be subject to estate recovery in states having a probate definition of estate, but would be included in states having a broad definition of estate for estate recovery purposes.

[1] I.R.C. §§ 673–677.

[2] I.R.C. §§ 1014, 2036, 2038; Treas. Reg. §§ 1.1014-2(a)(3), (b).

The post TAX AND ESTATE RECOVERY ISSUES IN CONNECTION WITH INCOME ONLY TRUSTS first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

Separate Trust

A separate trust designed specifically to control the retirement account is recommended. It is best that the trust not be part of a revocable living trust or any other trust. A “standalone retirement trust” is preferred.

Professional Trustee

When an IRA is paid to a standalone retirement trust or any other trust, it is important to consider a professional trustee. The rules regarding inherited retirement accounts are complex and family member trustees are often unfamiliar with them. This could cause a loss of important tax benefits. Most family members do not understand the rules regarding required minimum distributions (RMDs), conduit trusts or accumulation trusts. This could cause loss of important tax benefits. If the retirement account is $500,000 or more, it usually makes more sense to name a professional trustee. The professional trustee understands the tax rules and has investment expertise.

A family member could be named as trust protector. A trust protector has the right to monitor the performance of the professional trustee and to remove and replace the trustee with another professional trustee, if the trust protector is not satisfied with the performance of the trustee.

Trust Protector

Under an IRA trust a trust protector can be appointed. The trust protector must be unrelated by blood to the trust beneficiary but may have a personal relationship, such as financial advisor, attorney, CPA, or friend. The trust protector can change a conduit trust to an accumulation trust. This gives the trustee the discretion to accumulate funds.[1]

Conclusion

As Americans rely less on the availability of work-related pensions for their retirement, more of their wealth is found in the tax-deferred retirement accounts that they have funded over the years. As the estate tax exemption grows and becomes less of a concern for most Americans, it becomes increasingly important to understand and plan for minimization of the income taxes that are ultimately payable with respect to these tax-deferred accounts while at the same time maximizing family wealth transfer goals. The standalone IRA Trust is sufficiently flexible that it allows most people to balance their tax and family goals well, offering opportunities for creditor and other beneficiary protections, protection for special needs beneficiaries and spousal planning as well as the possibility of professional management to assist in investing and minimizing income taxes for the beneficiaries.

[1] P.L.R. 200537044; Harvey B. Wallace, II, Retirement Benefits Planning Update, Probate and Property, American Bar Association (May-June 2006); Wealth Preservation Update, Morris Law Group (Mar. 2007), www.law-morris.com.

The post RETIREMENT ACCOUNT TRUSTS – Part 2 first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

Introduction

The United States Supreme Court in a 9-0 unanimous ruling held that an inherited IRA is not protected in bankruptcy under federal law.[1] Heidi Heffron-Clark inherited an IRA from her mother in 2001 and filed for bankruptcy nine years later. The court held that the IRA was not shielded from her creditors, because the funds were not earmarked exclusively for retirement. The Supreme Court indicated that creditor protection does not apply to inherited IRAs for a number of reasons:

- Beneficiaries cannot add money to an inherited IRA like IRA owners can to their accounts;

- Beneficiaries of inherited IRAs must generally begin to make Required Minimum Distributions (RMDs) in the year after they inherit the accounts regardless of how far away they are from retirement;

- Beneficiaries can take total distributions of their inherited accounts at any time and use the funds for any purpose without a penalty. IRA owners must generally wait until age 59-1/2 before they can take penalty-free distributions.

The court held that inherited IRAs do not contain funds dedicated exclusively for use by individuals during retirement. As a result, the favorable bankruptcy protection afforded to retirement funds under the Federal Bankruptcy Code does not apply.

The court did not rule on whether a Spousal Rollover IRA is protected from creditors. Like other IRA owners, if the money is rolled into their own IRA, they may have to pay a 10% early-withdrawal penalty if money is taken before age 59-1/2. If the money is not rolled over into the Spousal Rollover account, then it would appear that the assets will not be protected in bankruptcy.

A way to safeguard IRA and other retirement account assets from creditors is to name a trust as beneficiary of the retirement account.

Trust as Beneficiary

- The best practice is to name a standalone retirement trust as beneficiary for IRAs and other tax-deferred retirement accounts. Naming a trust as beneficiary provides more control. A trust can be drafted to protect the assets from a beneficiary’s creditors.

- If retirement account monies are left directly to heirs, the funds may be squandered by the heirs defeating any benefit of the long-term tax deferral. The trust provides protection from premature withdrawal.

- If the heir is divorced, the retirement account funds may be subject to claims of the non-heir spouse, or if the IRA is in a trust, the non-heir spouse will not be able to attach them.

- Benefit of Beneficiary. If a parent names a child as beneficiary of the parent’s retirement account and subsequently the child dies, that child may name the child’s spouse as beneficiary and the child’s spouse may remarry naming the new spouse as beneficiary. The retirement account would no longer remain in the bloodline. The trust can be designed so that on the death of the child the account passes to other family members and is kept in the bloodline.

- Special Needs. If the beneficiary has special needs, the trust can be drafted to protect the beneficiary’s entitlement to government programs such as SSI, Medicaid or any other means-tested public benefits.

- Finally, if the funds are placed in a trust no guardianship proceeding is needed upon the beneficiary’s incapacity.

[1] Clark v. Rameker, 134 S. Ct. 2242 (2016).

The post RETIREMENT ACCOUNT TRUSTS – PART 1 first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

For many years a debate has raged as to whether Medicare’s interests must be considered with respect to future medical payments in the context of a third party liability settlement (“TPLS”). The issue is simple. If a plaintiff in a TPLS receives money to pay for future medical care, is he free to pocket that money and send the bill for the future medical care to Medicare? Under the Medicare Secondary Payer Act (“MSPA”), Medicare is prohibited from making a payment for future medicals to the extent that such payment has been made under liability insurance. Therefore, if a liability insurance company or self-insured defendant pays money to a plaintiff for future medical care, the argument goes that Medicare cannot pay for that care.

In 2013, the Centers for Medicare and Medicaid Services (“CMS”) issued a Notice of Proposed Rulemaking (“NPRM”), but then voluntarily withdrew it in 2014. As a result, parties have been left to their own devices in determining how to address this issue. Some commentators believe that absent enforceable regulations that identify the standards by which future medicals are to be measured in the liability context, the federal government has no right to claim an interest in future medicals as part of the settlement. On the opposite end of the spectrum, commentators observe that CMS interprets the MSPA so that it is applicable to TPLS as well as Worker’s Compensation claims. The correct position may lie somewhere in between. The real answer may be to develop an analysis of how much of the TPLS was for future medicals and how much for other elements of damages and to set the future medical money aside, so that Medicare is not billed until that portion of the settlement is exhausted.

Once a Medicare Set-Aside Arrangement (“MSA”) has been considered, the next question is how much is necessary to fund it. If future medicals have been plead or claimed and future medicals are specifically released in a Release signed in connection with the third party liability (“TPL”) settlement, then it is likely that Medicare’s interests must be considered. That raises the question as to how to calculate the amount of the settlement intended for future medical care. It is unlikely that CMS would accept a figure agreed upon by the parties absent court testimony and a court finding.

It is important to remember that in a TPL case, the award seldom pays 100 cents on the dollar for future medicals. Issues in these cases, such as disputed liability or causation, policy limits, statutory caps and derivative claims, often mean that TPL cases are resolved for less than the full measure of damages sustained. The Garretson Resolution Group recommends a starting point for a maximum amount may be identified through review of a plaintiff’s life care plan and other evidence of the dollar assigned to particular damages other than future medicals. These would include procurement costs, liens, past medicals, pain and suffering, loss of future earning capacity, etc. Garretson outlines a four-step process:

- Were future medicals plead or released as part of the settlement, judgment or award?

- Does the plaintiff require future injury-related care?

- Does the settlement award “compensate” plaintiff for future medicals based on objective decisional future medical allocation methodology?

- How much did the settlement award compensate based on objective decisional future medical allocation methodology?

By analyzing the settlement to figure out how much would be appropriate for future medicals and then determining the ratio of the plaintiff’s net proceeds to the total damages, a percentage for future medicals can be determined. This is the amount “compensated” for future medicals within the settlement or award. This would only be the amount necessary to set aside to satisfy CMS.

This approach is different from the traditional approach. The traditional approach to funding an MSA is to determine what the future medical costs to be paid by Medicare would be and set that money aside without regard to whether the plaintiff actually recovered that amount for future medicals. Under the Garretson approach, the only amount to be set aside would be the actual funds recovered by the plaintiff, which could be considerably less than the total future medicals.

Once the amount of the MSA has been determined, who shall administer those funds? One option is to use a professional custodian such as Medi-Vest. The advantage to the professional custodian is that they know the rules. They use the set-aside funds only to pay for medical care that Medicare would cover. The plaintiff may be receiving other medical care that would not be covered by Medicare and use of the MSA funds for payment of that care would be inappropriate. A professional custodian will also take advantage of the discounts offered to Medicare, rather than paying full retain prices. This makes the funds last longer. The other option is to turn over the MSA amount to the plaintiff to be self-administered. The advantage to this approach is that it avoids paying the professional custodian’s fees. There is usually a set-up fee and an annual maintenance fee. A disadvantage to a self-administered MSA is the plaintiff does not know the rules and often uses the funds for other purposes such as covering delinquent mortgage payments or payments on car loans. As a practical matter, if the Set-Aside is a $100,000 or more, it usually makes sense to engage the services of a professional custodian. If the settlement is less than $100,000, the cost of a professional custodian are not warranted and a self-administered MSA is more appropriate.

The next consideration for an MSA is whether or not a Structured Settlement should be considered. CMS requires that an MSA be funded with a lump sum sufficient to cover two year’s medicals plus the first surgery, but the rest can be funded with a Structured Settlement. Since most of the funds will not be needed right away, it often makes sense to use the Structured Settlement. Statistics show that where a Structured Settlement is used, the cost is only 52% of funding an MSA with a lump sum. This is because the Structure does not have to pay out for a period of time. The Structure can also take advantage of the plaintiff’s rated age.

The post DO WE STILL NEED TO WORRY ABOUT MEDICARE SET-ASIDE ARRANGEMENTS? first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

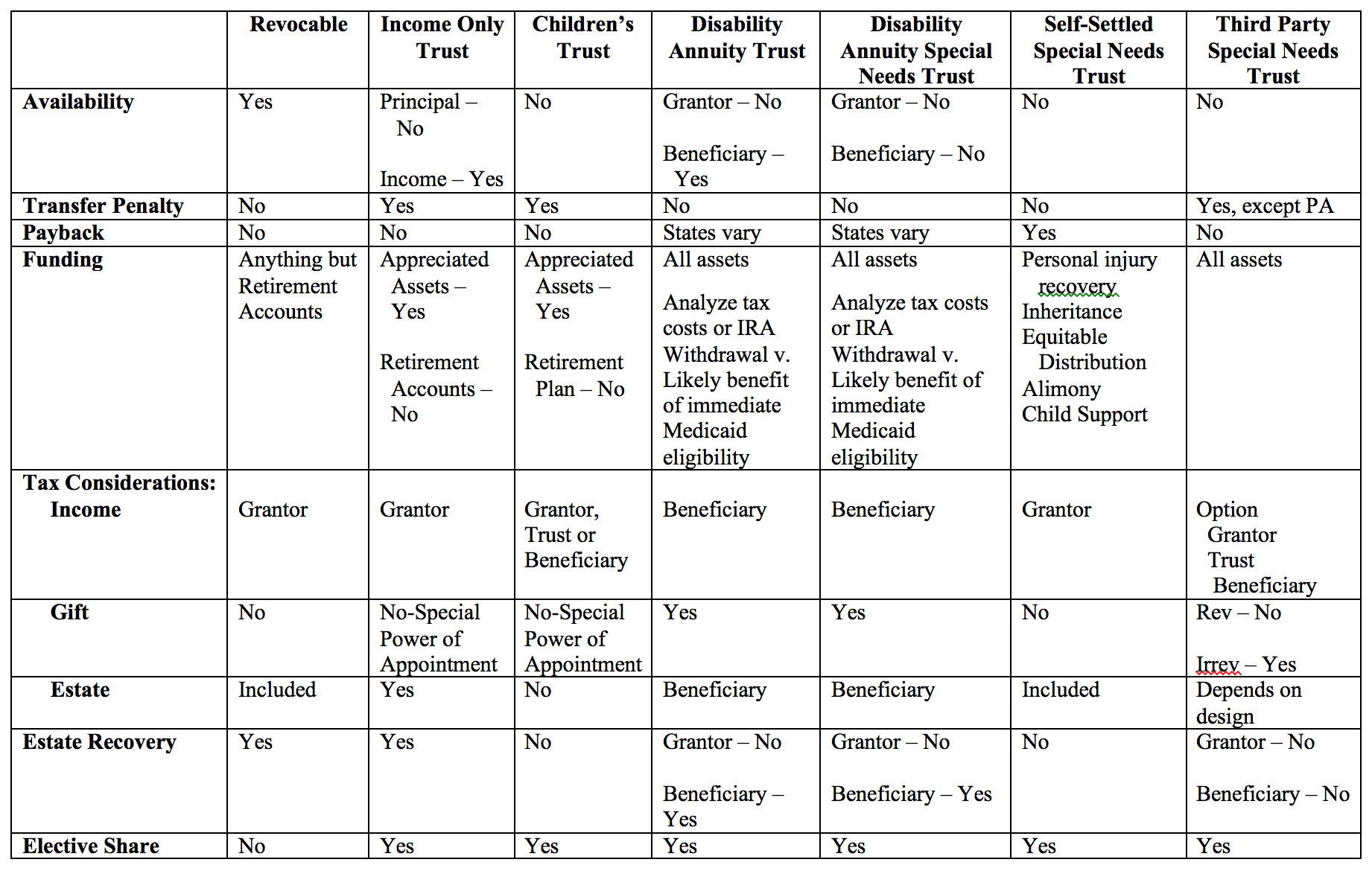

There are seven Trust that should be addressed in considering Medicaid. These are: Revocable Trusts, Income Only Trusts, Children’s Trusts, Disability Annuity Trusts, Disability Annuity Special Needs Trusts, Self-Settled Special Needs Trusts, and Third Party Special Needs Trusts.

There are seven considerations in drafting trusts. These are: availability of trust assets, applicability of a Medicaid or SSI transfer penalty, Medicaid payback provisions, good and bad assets for funding trusts, tax considerations (including income, gift and estate), estate recovery, and elective share issues. This chart is designed to address each of those issues with each of those trusts at a glance.

by Thomas D. Begley, Jr., CELA

Types of Trusts. Trusts established and funded after August 10, 1993, are governed by OBRA-93. The Medicaid-qualifying trust rules were repealed by OBRA-93, and new rules for revocable and irrevocable trusts created after August 10, 1993, were established. OBRA-93 also created special disability trusts, each of which has rules. These trusts include Self-Settled Special Needs Trusts and Pooled Trusts. OBRA-93 also established a Miller Trust, to be used when a potential Medicaid recipient has income in excess of the income cap. The fourth trust authorized under OBRA-93 is a sole benefit of trust.

The commonly-used trusts in Medicaid Planning include the following:

- Income Only Trust

- Children’s Trust

- Disability Annuity Trust

- Disability Annuity Special Needs Trust

- First-Party Special Needs Trust

- Third-Party Special Needs Trust

What Constitutes a Transfer. The key to understanding the transfer rules pertaining to trusts is to understand when the transfer has taken place. If there is a transfer from an individual then to a trust under conditions by which the trust assets are still available to the individual, for Medicaid purposes there has been no transfer. Therefore, where the trust is revocable, the assets are still available to the individual after the trust is funded so there is no transfer at this point. The transfer is considered to have taken place on the date of payment from the trust to a third party.

If the trust is irrevocable, the transfer is considered to have been made as of the date the trust was established and funded, or upon such later date that payment to the settlor was foreclosed. However, if the settlor can still benefit from the assets with which the trust is funded, those assets are still available so there is no transfer. If and when those assets are paid out to a third party, the transfer occurs. If the settlor places assets in an irrevocable trust and can no longer benefit from any of the trust corpus, there has been a transfer of assets when the trust is funded.[1]

Drafting Considerations for Trusts. There are seven main issues to be considered in drafting any trust involving a potential Medicaid recipient. These considerations are:

- Availability

- Transfer of asset penalty

- Payback provision

- Funding

- Tax considerations, including income, gift and estate

- Estate recovery

- Elective share

[1] 42 U.S.C. § 1396p(c)(1)(B); HCFA Transmittal 64 § 3258.4E.

The post OVERVIEW OF MEDICAID TRUSTS first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

Once a Medicare Set-Aside Arrangement (“MSA”) has been considered, the next question is how much is necessary to fund it. If future medicals have been plead or claimed and future medicals are specifically released in a Release signed in connection with the third party liability (“TPL”) settlement, then it is likely that Medicare’s interests must be considered. That raises the question as to how to calculate the amount of the settlement intended for future medical care. It is unlikely that the Centers for Medicare and Medicaid Services (“CMS”) would accept a figure agreed upon by the parties absent court testimony and a court finding.

It is important to remember that in a TPL case, the award seldom pays 100 cents on the dollar for future medicals. Issues in these cases, such as disputed liability or causation, policy limits, statutory caps and derivative claims, often mean that TPL cases are resolved for less than the full measure of damages sustained. The Garretson Resolution Group recommends a starting point for a maximum amount may be identified through review of a plaintiff’s life care plan and other evidence of the dollar assigned to particular damages other than future medicals. These would include procurement costs, liens, pain and suffering, loss of future earning capacity, etc. Garretson outlines a four-step process:

- Were future medicals plead or released as part of the settlement, judgment or award?

- Does the plaintiff require future injury-related care?

- Does the settlement award “compensate” plaintiff for future medicals based on objective decisional future medical allocation methodology?

- How much did the settlement award compensate based on objective decisional future medical allocation methodology?

By analyzing the settlement to figure out how much would be appropriate for future medicals and then determining the ratio of the plaintiff’s net proceeds to the total damages, a percentage for future medicals can be determined. This is the amount “compensated” for future medicals within the settlement or award. This would only be the amount necessary to set aside to satisfy CMS.

This approach is different from the traditional approach. The traditional approach to funding an MSA is to determine what the future medical costs to be paid by Medicare would be and set that money aside without regard to whether the plaintiff actually recovered that amount for future medicals. Under the Garretson approach, the only amount to be set aside would be the actual funds recovered by the plaintiff, which could be considerably less than the total future medicals.

The post HOW MUCH MUST BE SET ASIDE FOR MEDICARE IN A THIRD PARTY LIABILITY CASE? first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

For many years a debate has raged as to whether Medicare’s interests must be considered with respect to future medical payments in the context of a third party liability settlement (“TPLS”). The issue is simple. If a plaintiff in a TPLS receives money to pay for future medical care, is he free to pocket that money and send the bill for the future medical care to Medicare? Under the Medicare Secondary Payer Act (“MSPA”), Medicare is prohibited from making a payment for future medicals to the extent that such payment has been made under liability insurance. Therefore, if a liability insurance company or self-insured defendant pays money to a plaintiff for future medical care, the argument goes that Medicare cannot pay for that care.

In 2013, the Centers for Medicare and Medicaid Services (“CMS”) issued a Notice of Proposed Rulemaking (“NPRM”), but then voluntarily withdrew it in 2014. As a result, parties have been left to their own devices in determining how to address this issue. Some commentators believe that absent enforceable regulations that identify the standards by which future medicals are to be measured in the liability context, the federal government has no right to claim an interest in future medicals as part of the settlement. On the opposite end of the spectrum, commentators observe that CMS interprets the MSPA so that it is applicable to TPLS as well as Worker’s Compensation claims. The correct position may lie somewhere in between. The real answer may be to develop an analysis of how much of the TPLS was for future medicals and how much was for other elements of damages. Then set aside only the amount received for future medicals, not the total anticipated costs of what the future medicals will actually be.

The post DO WE STILL NEED TO WORRY ABOUT MEDICARE SET-ASIDE ARRANGEMENTS? first appeared on SEONewsWire.net.]]>

by

Thomas D. Begley, Jr., CELA

Below is a chart comparing an ABLE Account with a Third-Party Special Needs Trust.

|

|

ABLE ACCOUNT |

THIRD PARTY SPECIAL NEEDS |

|

Onset of Disability |

Qualifying to

|

No |

|

Age of Beneficiary

|

No |

No |

|

Who May Establish

|

Beneficiary, |

Anyone |

|

Number of Accounts

|

One |

Unlimited |

|

Fees

|

Financial |

Attorney |

|

Contribution Limits |

$14,000 for SSI total

|

Unlimited |

|

Investment Options |

Investment

|

No |

|

Valid Distributions |

Broadly |

Any

|

|

Taxes |

Earned |

Can

|

|

Medicaid Payback Upon Death of

|

Remaining for Medicaid benefits. |

No |

The post ABLE ACCOUNT, THIRD PARTY SPECIAL NEEDS TRUST AND POOLED TRUST: COMPARE first appeared on SEONewsWire.net.]]>

by Thomas D. Begley, Jr., CELA

New Jersey has now enacted the Achieving a Better Life Experience Act (“ABLE”). It is understood that by Fall this Act will be ready for implementation. The question will then remain: “What is the best option? Should the parent intending to set aside money for a child with disabilities establish an ABLE account or a Third Party Special Needs Trust?” Generally speaking, if the individual would be the beneficiary became disabled prior to attaining age 26, then an ABLE account might be considered, if the account will be small. There is very little point to establishing an ABLE account for a significant amount of money. There are two primary advantages to an ABLE account: (1) the income builds up tax free, and (2) the cost of establishing and administering the account is relatively small. The disadvantage is that on the death of the beneficiary any funds remaining in the account must go first to repay Medicaid for medical assistance paid during the beneficiary’s lifetime.

Therefore, it would seem that if the account is to be relatively small (i.e., $25,000), an ABLE account might make sense. However, once the account exceeds that amount it probably makes more sense to transfer the funds to a Pooled Trust Third-Party Subaccount. While there is a set-up fee and administrative costs, there are also benefits and there is no Medicaid payback. For accounts between $25,000 and $100,000, a Pooled Trust probably makes more sense. This is true even though the Pooled Trust does not enjoy the advantage of tax-free income. The truth of the matter is that on an account of $100,000, the income tax savings is minimal. The beneficiary is also usually in a low tax bracket.

Once the account exceeds $100,000, a Third-Party Special Needs Trust probably makes sense. Yes, there are costs of establishing and administering the trust, but there is no Medicaid payback on death. Once an ABLE account reaches $100,000, the beneficiary’s Supplemental Security Income (“SSI”) is suspended. If the funds are in the Third-Party Special Needs Trust, SSI remains in effect. Between the benefit of the SSI payment and the advantage of no Medicaid payback, the cost of establishing and administering the Third-Party Special Needs Trust probably makes the most sense.

The post SPECIAL NEEDS TRUST, POOLED TRUST OR ABLE ACCOUNT: WHAT IS MY BEST CHOICE? first appeared on SEONewsWire.net.]]>

by Thomas D. Begley, Jr., CELA

New Jersey has passed the Achieving a Better Life Experience ACT (“ABLE”). While the Act has passed, it will take some time to implement. Many commentators believe that by Fall accounts will be able to be opened.

Under the ABLE Act, people with disabilities and their families may set up special savings accounts similar to 529 Plans to be used for disability-related expenses. Earnings on these accounts are non-taxable. Generally, if the fund does not exceed $100,000, it will not be counted for Supplemental Security Income (“SSI”) purposes. If the fund exceeds $100,000 then SSI will be suspended, but Medicaid can be continued so long as the total amount in the account does not exceed the amount authorized for 529 Plans. To be eligible, an individual must become disabled prior to age 26 and be disabled. If the individual receives Supplemental Security Disability Income (“SSDI”) or SSI or files a Disability Certification under IRS Regulations, she will be considered disabled.

Funds can be used for education, housing, transportation, employment training, support, assistive technology, personal support services, health, prevention and wellness, financial management and administrative fees as well as legal fees and expenses for oversight and monitoring.

The total amount contributed to an ABLE account in any one calendar year by all contributors cannot exceed the amount of the federal annual gift tax exclusion, which for 2016 is $14,000. The drawback to these accounts is on the death of the account owner, any funds remaining in the account must be used to repay Medicaid for any funds advanced on behalf of the account holder. The best strategy seems to be to use these accounts for small gifts. Normally, these accounts would be used for gifts from parents. As long as the gifts are less than $14,000 per year and do not accumulate very much, these accounts might make sense. However, because of the Medicaid payback, it does not make sense to have these accounts grow. A Third Party Special Needs Trust is a much better option, if the amount involved is significant.

The advantages of an ABLE account are the tax-free income. However, realistically this is not a significant advantage because the income on small accounts is low and the other income of the beneficiary with a disability is usually low, so the tax saving sounds more attractive than it actually is. The other advantage is that there is a minimal cost to establishing the account when compared to establishing a Pooled Trust or a Third Party Special Needs Trust.

The disadvantages are the Medicaid payback and the possible loss of SSI. Because of the Medicaid payback, it makes little sense to build up a large account. The SSI benefit of approximately $750 per month is a significant benefit that should be protected.

Ideally, ABLE accounts appear to be useful if they are in the $25,000 to $50,000 range, but not for larger accounts. A Pooled Trust or Special Needs Trust would be more appropriate.

The post ABLE ACCOUNTS ARE COMING TO NEW JERSEY first appeared on SEONewsWire.net.]]> I don’t know everything, what I do know is that I have a deep level of knowledge in very few areas of law and financial planning. When it comes to estate planning concepts as it applies to Main Street (not Wall Street) families who are interested in protecting what they’ve worked hard to earn, I’d put my pedigree and knowledge up against any other estate planner or financial planner. That said, in other areas of law, unless I saw it on Law & Order last night, I’m not going to know it….and I’m happy to admit that I don’t know.

I don’t know everything, what I do know is that I have a deep level of knowledge in very few areas of law and financial planning. When it comes to estate planning concepts as it applies to Main Street (not Wall Street) families who are interested in protecting what they’ve worked hard to earn, I’d put my pedigree and knowledge up against any other estate planner or financial planner. That said, in other areas of law, unless I saw it on Law & Order last night, I’m not going to know it….and I’m happy to admit that I don’t know.

That last part is the most important thing. I don’t pretend to know or dismiss things I don’t know enough about, I either learn them or accept that I don’t know. That’s how I got into elder law in the first place. I was a pure estate planning attorney, focusing on what happens when you pass away. But I was being bombarded with questions revolving around “what happens if I don’t pass away and continue to age, then what?” I didn’t have the answer, didn’t pretend to have the answer, so I dove deep into the laws and strategies to become an expert on that answer. Going on to become the second youngest attorney at the time to pass the Certified Elder Law Attorney exam in the nation and become the 15 CELA in the state of Michigan. Then going on to write a book on the subject and then teach Elder Law at WMU Cooley Law School.

Who Do You Trust for Heart Surgery? Heart Surgeon or Family Doctor?

If you are going in for heart surgery would you want the experienced heart surgeon or would you trust your family doctor when it comes to performing the surgery?

Likewise, I’m surprised when families get a second opinion from a financial planner or family lawyer when it comes to our recommendations. We then end up having to educate the family lawyer or financial planner on Medicaid, Medicare, Tax Law, Veterans Benefits, Asset Protection rules, Trust rules, beneficiary designations, etc…

I’m happy to do it, but I just feel for the families who are often mislead when it comes to asset protection by lawyers and financial planners who know enough to be dangerous…and often are.

When it comes to planning to protect you legally from the devastating cost of long-term care are you going to have more faith in a Certified Elder Law Attorney (CELA), who teaches elder law to law students as an adjunct professor, written a book on the subject, teaches continued education to lawyers and financial planners on the topic or an annuity salesman or basic estate planning attorney? I welcome the opportunity to educate the professional on the planning strategies–they often turn into wonderful referral sources.

Price Shop Your Heart Surgeon? Documents versus Planning.

Would you price shop your surgeon? Do you want the cheapest heart surgeon you can afford? Probably not. The difficult thing to understand with good legal estate planning is that not all documents are created equal. If you call up 10 attorneys and ask how much a trust costs, you’ll get varying answers. You can have a trust done online for probably $40 or you can have an estate plan done for free through UAW Legal Plan, if you’re a member. But the age old lesson applies….you get what you pay for. That applies to legal planning as well.

Having a trust or power of attorney isn’t enough. It’s what that document says. Better than that is how those tools are used. If I asked you to get me a paint brush, would you know what type of brush to get me? It’s all about the planning.

Their Ego Versus What’s Best For You

Sometimes, not all the time, there are financial planners or other attorneys who feel like that if they are not familiar with a strategy or haven’t heard of a certain type of trust, that it a) doesn’t work or b) isn’t right for you. This is just their ego getting in the way of what is best for you. You look up to them as a trusted advisor and they may feel that by having a new strategy (asset protection isn’t new, by the way…), it challenges their authority and the respect you may have for them.

This is very closed minded of the advisor and can be detrimental to your planning.

I love working with open minded lawyers and advisors. In fact, just last week I was having coffee with an advisor at one of the Wall Street type financial planning firms and he said to me “Chris, this is amazing, can you come present to my group?” Of course. This is the point, share ideas for what’s best with your clients. Not all planning is right for all clients, but at least know the options out there.

Sure, you can do a basic trust that avoids probate (if funded properly) and controls assets upon death. But you can also build an asset protection trust that does all that PLUS protects you. Get educated. Know your options. Choose a plan that works for you.

The post What Your Financial Planner or Family Lawyer Doesn’t Know, Hurts You! appeared first on Michigan Estate Planning.

The post What Your Financial Planner or Family Lawyer Doesn’t Know, Hurts You! first appeared on SEONewsWire.net.]]>by Thomas D. Begley, Jr., CELA

Historically, a member of the military could arrange for a pension and provide a survivor’s benefit to a spouse or child. A problem arose where the child had a disability and was receiving means-tested public benefits such as Supplemental Security Income (“SSI”) or Medicaid. If the child with disabilities receiving those benefits or other means-tested public benefits received the pension, they would lose the benefits. This is because any income received from any source reduces the SSI income dollar-for-dollar, and if the pension exceeded the amount of SSI income, SSI would be completely lost. Medicaid is frequently linked to SSI, so that if SSI is lost, the Medicaid would be also be lost. What follows is a story of the Power of One.

An Elder and Disability Law attorney in Virginia, named Kelly Thompson, took up the cause of these beneficiaries with disabilities. Kelly enlisted help from the Special Needs Alliance, which is a national organization of lawyers practicing in the disability field and also the National Academy of Elder Law Attorneys. After several years of hard work, in late 2014 Congress enacted the Disabled Military Child Protection Act in the 2015 National Defense Authorization Act. This legislation allows military retirees and service members to designate their survivor benefit to a Special Needs Trust for the benefit of their disabled child or children.

By having the survivor pension benefits irrevocably paid into a Special Needs Trust, those funds are not counted in determining the financial eligibility of the disabled child. The net result is that the military member’s or retiree’s children with disabilities are able to benefit from the pension as well as maintain their vital public benefits.